AAPL 2Q12 Estimate

- I expect iPad and iPhone to represent approximately 75% of Apple’s quarterly revenue.

GM: 42.9% (AAPL guidance: 42%/Consensus: 42.7%)

- Apple’s margin jumped to 44.7% last quarter, from 40.5% in 2011. Continued strong iPhone sales should benefit overall GM in 2Q12, with attractive component pricing providing additional support.

EPS: $11.45 (AAPL guidance: $8.50/Consensus: $9.81)

- I expect Apple to report 79% yoy EPS growth, which is slightly less than the 83% yoy EPS growth observed in 2011.

Product Unit Sales and Commentary

Macs: 4.3 million (14% yoy growth)

- With no Mac updates during the quarter, I expect Mac shipments to show continued yoy growth, albeit at a slower pace than 1Q12. iPad cannibalization is also picking up as consumers bypass Macs for lower-priced iPads.

iPad: 12.0 million (155% yoy growth)

- Apple sold three million new iPads during opening weekend (includes pre-orders that shipped for the 12 days leading up to the March 16 launch, but not iPad 2 sales). My iPad estimate is primarily based on weekly sales run rates, using Apple’s new iPad opening weekend sales as a benchmark between slower iPad sales in January and February and the supply/demand imbalance at the end of March. Unlike last year’s iPad launch, Apple seemed to have a better handle with new iPad supply, as online shipment waits did not reach 2011 levels, even with a more extensive international rollout. My estimate assumes approximately 6 million new iPads sold during the last 3.5 weeks of March and an additional 6 million iPads sold in January, February, and the beginning of March.

iPod: 6.8 million (25% yoy decline)

- Representing only 2.7% of estimated 2Q12 revenue, the iPod is a footnote.

iPhone: 36.4 million (95% yoy growth)

- My estimate reflects an average 2.2 million weekly sales run rate and the addition of approximately 6 to 8 million iPhones into the distribution channel (approaching Apple’s desired 4 to 6 week range). For some perspective, Apple saw a 1.6 million weekly iPhone sales run rate during 2Q11 (pre-iPhone 4S). My 2Q12 estimate assumes 38% yoy growth in the weekly run rate, which I think is reasonable given the iPhone 4S and increased iPhone penetration at newer carriers (including Verizon and Sprint) and countries (China).

When Apple releases earnings on April 24, many will look at iPad and iPhone sales as an indicator for continued strong consumer demand. I suspect Apple may be allowed some breathing room on iPad sales given the supply/demand imbalance and trickiness surrounding a new product launch. Meanwhile, iPhone lacked any significant interferences during the quarter, with results dependent on demand, and to a lesser extent, the number of units added into the distribution channel.

Thoughts on the new iPad

Software and Hardware

Why has iPad been so successful? Intriguing software? Gorgeous hardware? After using iPad 2 for a year, my connection with the device has been formed by the seamless interaction between software and hardware. The iPad form factor seemingly disappears as I interact with iOS apps. Meanwhile, iPad competitors have focused on only one aspect of the software & hardware duplex; either shipping okay software (“okay” can be an overstatement) with mediocre hardware, or okay hardware (again, I am being generous) with buggy software. The new iPad’s improved hardware features, along with new apps, combine to form a package that can appear to be “magical” to the user.

Motorola RAZR Syndrome

One of the bigger risks Apple faces is the “Motorola RAZR Syndrome”, or reliance on your current success at the detriment of your future success. After three generations of iPads, it is clear that Apple understands its biggest competitor is Apple. The new iPad’s biggest competition will come from iPad 2, while the original iPad was iPad’s 2 biggest competitor. Even though the original iPad sold well, Apple continued to push the envelope with iPad 2, and now the same can be said with the new iPad. Cameras, a Retina display, faster guts, amazing software, improved battery life, and 4G LTE, all at the same $499 entry-level price point.

iPad 2 Price Drop

Although Apple devoted only a brief minute to iPad 2’s new $399 price, consumers will give the $100 price drop much more attention. For many, price remains king. While $399 is still a lot of money, consumers are starting to compare iPad to regular laptops, in which the $399 price tag doesn’t look nearly as steep. Similar to the iPhone 3GS and iPhone 4 being bought by former feature phone owners, the iPad 2 will continue to sell well as laptop owners look at iPad for the first time.

More iPads in the Wild?

Up to now the iPad had been looked at as largely an “inside the home” device, confined to the living or play room. With the original iPad not having any cameras, using an iPad at a social event, such as a family occasion, picnic, or concert, was questionable. Apple’s new video and picture software (and improved cameras) will give people a greater incentive to bring iPad to different gatherings and events. While iPad is still no where near as convenient to transport as iPhone, it is easier to transport than any other computing device. As more iPads find their way into the wild, a whole new marketing realm will kick in. While advertisements can be effective, seeing friends or family enjoy their iPad outside the confines of their home represents a brand new marketing angle.

Jony Ive and New Product Form Factors

The new iPad’s form factor has subtle differences from iPad 2 (the minor variances might even be hard for a normal consumer to see or feel). While Apple’s SVP of Industrial Design, Jony Ive, is intimately involved in any form factor change, no matter how minuscule, my gut tells me we might see some interesting new form factors for most, if not all, of Apple’s product lines over the next year. I think this is what Tim Cook hinted at at the end of the new iPad’s unveiling when he said, “Across the year, you’re going to see a lot more of this kind of innovation. We are just getting started.” What is the point of changing form factors that seemingly don’t need to be fixed? How much can you change a phone or tablet form factor? Apple doesn’t settle. New product form designs will focus on greater functionality and feasibility, all while keeping design at the forefront. Dimension barriers will be dismantled. A new round of product design and manufacturing innovation is on the horizon and Jony is guiding the ship.

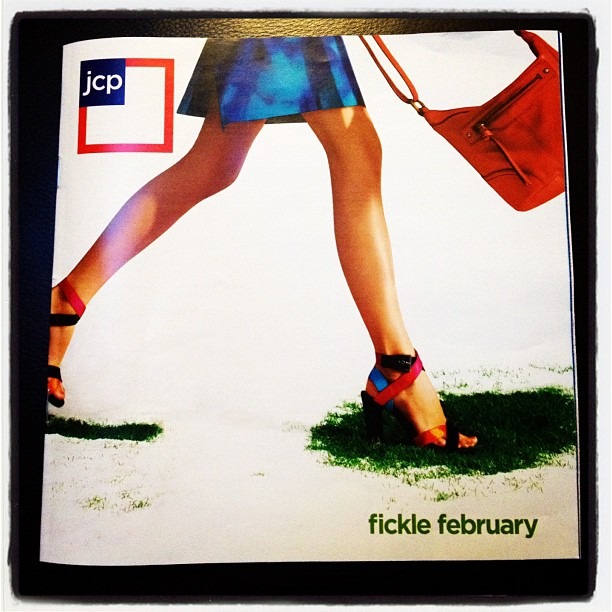

Transferable Traits

A: Proof that the Apple Way is a transferable trait.

Q: What is Former Apple SVP Ron Johnson’s new JCP Sunday circular?

- Let the product do the talking

- Less is more

- Spend more timing looking ahead than behind

- Know when to place a big bet, and then go all in.

Not Everyone Copies Apple

"[Apple is] going to continue to make the best products in the world that delight our customers and make our employees incredibly proud of what they do."

- Tim Cook in his first email to Apple employees as Apple’s new CEO sent August 25, 2011

"The path [Sony] must take is clear: to drive the growth of our core electronics businesses - primarily digital imaging, smart mobile and game; to turn around the television business; and to accelerate the innovation that enables us to create new business domains."

- Kazuo Hirai in response to being appointed Sony’s new President and CEO on February 1, 2012

Apple: {best, world, delight, proud} vs. Sony: {growth, businesses, accelerate, domains}

Not everyone copies Apple.

Apple 1Q12 Preview: Tale of Two Products

Apple’s 1Q12 earnings report will boil down to two simple data points: iPhone and iPad sales. Guidance will take a back seat, as will margin expectations and management commentary. The market wants confirmation that iPhone and iPad demand is robust, especially after Apple’s disappointing 4Q11.

The magic numbers will be 31 and 13. If Apple sold more than 31 million iPhones and 13 million iPads, Apple will have met expectations (sky-high for iPhone and lukewarm for iPad). Whisper numbers (the numbers that analysts secretly discuss) probably stand somewhere near 34 million iPhones and 15 million iPads, but missing whisper numbers usually won’t lead to negative EPS estimate revisions.

In an attempt to put the last few weeks of heightened iPhone 1Q12 expectations (and reduced iPad expectations) within context, and using my 1Q12 estimates published on November 18, 2011, I would put 27 million iPhones and 12 million iPads as the minimal bar Apple has to jump over in order to avoid significant negative EPS revisions and price target cuts.

Incompetency

Research in Motion (RIMM) is in a death spiral. Consumers are moving away from the platform in droves, Blackberries have lost the “cool” factor, and RIMM management is unable to control Wall Street expectations. RIMM’s primary problem is incompetent management.

At first, it is difficult to believe that such a large company (at least in the eyes of Canada) could possibly have inept management. People assume if you are CEO of a company, you know what you are doing. How else would you get to the top position of a multi-billion dollar company?

Unfortunately, RIMM management is indeed inept and incompetent. RIMM understands its main problem; no one wants the current Blackberry phone line-up. Don’t be fooled by RIMM sales figures still in the millions of units. Quarterly sales are declining in absolute terms (in a market that is booming). A bad sign to say the least. However, RIMM doesn’t know the solution to its problem. According to RIMM, the solution is introducing new Blackberries. Take the Blackberry that everyone loved, and just give it incremental updates or speed bumps. Problem solved. You can see how this solution is inadequate and simply wrong. According to management, RIMM is facing hard times because Blackberry updates are delayed (It’s hard to recall a moment when RIMM management actually admitted things aren’t going well - a tell-tale sign that incompetency is running the show). Management is living in a fairy tale where iOS and Android aren’t the problem. Some may say that RIMM knows it has no viable solution to compete against iOS and Android. If true, I don’t see how the current management team and Board are still working for RIMM shareholders. It speaks volumes that not even activist shareholders want to get involved in RIMM…yet.

Making matters worse, RIMM is now unable to push out new Blackberries until the end of 2012. I assume RIMM employees are still going into the office each day and doing something. The question is what exactly are they doing?

How did RIMM get in this position? I suspect the timeline went something like this:

1) iPhone is introduced. 2007.

RIMM laughs it off and is confident that RIMM sales won’t be impacted. iPhone doesn’t have a physical keyboard. Who would want that?

2) Significant iPhone updates are introduced, including the app store. Android begins to take off (largely resembling iOS - apps and touch screens). 2008 and Early 2009

RIMM sales are still growing and RIMM’s stock price hits an all-time high in the middle of 2008. The subsequent global financial crisis hits RIMM’s stock price (along with every other company) masking some of the growing issues around the company.

3) iPhone and Android are exploding. Middle to Late 2009.

Up to this point, I really don’t think RIMM was too concerned with its prospects. Consumers (enterprise) were still addicted to Blackberries and its email capabilities and physical keyboards. Fundamental holes are forming though. ASPs are beginning to fall and RIMM is starting to lose grip of the high-end market. Channel fill is at all-time highs. Developed country growth is no longer increasing. Management’s solution is to focus on emerging markets. Problem solved.

4) iPhone 4. 2010.

The game has changed - again. RIMM has to see signs that things are not going well. iPhone blows past RIMM in sales. RIMM introduces its flawed Playbook. RIMM’s plan for phones? Updated Blackberries, of course. Research and development is caught flat-footed and asleep. RIMM has little to nothing in terms of alternatives beyond its signature Blackberry keyboards.

5) Current Day.

Playbook is a disaster. RIMM is in a death spiral. Incremental updates are now in disarray. iPhone and Android are eating up RIMM’s marketshare.

RIMM will make a classic business school case study. RIMM was a company that became a powerhouse for doing one thing really well (email) at a time when the smartphone market was a disaster and phones really weren’t too smart. Apple introduced the iPhone and everything changed. Even though many of RIMM’s metrics appeared healthy (subscriber growth, increasing sales) for a number of quarters post-iPhone, tumors were forming. Consumers were offered a better alternative and RIMM was unable to respond due to their inability (or lack of desire) to move beyond its core competency and lead the market into new innovation.

RIMM now faces a number of severe and multifaceted problems that could very well lead to the end of the company. I don’t think RIMM R&D is capable of innovating. RIMM has already lost the cool factor and chances are slim they will ever get it back. RIMM management seemingly never planned for the product after Blackberry. I don’t think its a stretch to think of it as Apple never planning for the day after the iPod. Sounds incomprehensible. Should companies that make such fatal errors, throwing innovation aside to instead milk current successes, deserve to survive? Even if RIMM does introduce a good phone in the future, consumers won’t care. If one thing is clear in consumer technology, it’s that momentum can be your friend (or in RIMM’s case, your enemy).

AAPL 1Q12 Estimate

I expect iPad and iPhone to represent nearly 70% of Apple’s quarterly revenue. My projected revenue is 38% higher than any previous quarter (closest was $28.6 billion revenue reported in 3Q11).

Apple’s margin in 2011 ranged from 38.5% to 41.7%. A higher iPhone mix during 1Q12 (including 3GS and 4 models) should benefit overall GM with component pricing remaining largely unchanged from previous quarters.

I expect Apple to report 63% yoy earnings growth.

Product Unit Sales and Commentary

Mac experienced 22% yoy growth in 2011 (34% growth in portables and 1% in desktops) and I expect similar growth during 1Q12 as consumers flock to the MacBook Air. Apple will continue to take market share from Windows (early stages of 5-10+ year trend). As the PC market struggles to grow (thanks in part to the proliferation of smartphones and iPad), I view long-term Mac growth near 10% as very respectable.

iPad supply/demand returned to equilibrium during 4Q11 with Apple reporting an average weekly sales rate of 925,000 iPads. My 14.7 million iPad estimate assumes an average 1.1 million iPad weekly (13 weeks) sales rate (higher than 4Q11 due primarily to holiday shopping). I am not forecasting any significant change to the iPad channel. While there have been many rumors and reports indicating softening iPad demand, I think some of that is the reduction of overly optimistic iPad expectations towards a more conservative consensus expectation. I think iPad will remain a top holiday gift. My 100% yoy growth does contain some conservatism when compared to 334% yoy iPad growth reported in 2011.

Continued strong iPod touch sales will partially offset the continued decline in Apple’s other iPod models. Apple refreshed the iPod line-up in 4Q11 and iPods do make great stocking stuffers, so my 15% yoy decline is slightly higher than the 20% and 27% yoy declines registered in 3Q11 and 4Q11, respectively.

iPhone 4S sales are off to a fast start with 4 million devices sold during opening weekend, a 1-2 week backlog on Apple’s online store (my iPhone 4S ordered from Apple took 15 days to arrive), and continued extended shipping waits at mobile carriers. It is clear that iPhone 4S supply/demand is not in equilibrium. iPhone 3GS (and iPhone 4) price reductions should also benefit 1Q12 sales. Apple’s largest iPhone quarter prior to 1Q12 was 20.3 million sold during 3Q11 (average of 1.7 million per week). My 28.4 million estimate reflects an average 2.2 million per week sales rate, but I admit that sales will be limited to Apple’s iPhone production levels. Another way to conceptualize my estimate: I am assuming 4 million iPhone 4S devices sold during opening weekend and then a subsequent 2 million units sold each following week (not out of the question given continued stockouts and the impact from 3GS and 4 models).

Questions can be addressed to me through twitter.

iPhone Accounted for Nearly 40% of U.S. Smartphone Sales in 3Q11

Nielsen’s third quarter survey of mobile users seemed to reaffirm what many have been saying; Android continues to grab more smartphone market share, with 43% U.S. share compared to iPhone’s 28%. This morning, I thought a little bit more about Nielsen’s data and something just didn’t seem right.

Since I follow AT&T’s and Verizon’s quarterly earnings, I recalled how AT&T’s most recent report indicated iPhone accounted for approximately 60% of AT&T’s smartphone sales. How was it possible that iPhone has less than 30% overall smartphone share in the U.S., while iPhone share at AT&T (the carrier with the highest smartphone penetration rate) is over 60%? After collecting a few more data points and running with conservative assumptions, I estimate that iPhone accounted for close to 40% of U.S. smartphones sold during 3Q11.

How Many Smartphones Were Sold in the U.S. During 3Q11?

One of my goals in this analysis was to rely on as little estimation as possible. In order to accomplish this, I was interested in only iPhone share (the rest of the mobile pie can be figured out at a later time). Fortunately, both AT&T and Verizon supply concrete iPhone and total smartphone sales data. During 3Q11, AT&T sold 4.8 million smartphones, of which 2.7 million were iPhones (56%). Meanwhile, Verizon sold 5.6 million smartphones, of which 2 million where iPhones (36%). Combined, iPhone accounted for 45% of smartphones sold at AT&T and Verizon during 3Q. What about Sprint and T-Mobile? Neither provide concrete smartphone sales data, primarily because they pail in comparison to larger competitors, AT&T and Verizon. Sprint indicated 8% of its 28 million postpaid ‘Sprint brand on CDMA’ subscriber base upgraded during 3Q, of which 80% were smart phone upgrades, which would lead to approximately 1.75 million smartphones sold during the quarter. With T-Mobile being much smaller than Sprint, I peg smartphone sales closer to 1 million. I assume that no unlocked iPhones made their way over to Sprint or T-Mobile during the quarter, which isn’t the case as T-Mobile recently indicated 1 million iPhones were are on their network (for comparison, T-Mobile has 10 million phones on its 3G/4G network).

iPhone’s Share of U.S. Smartphones Sales

Running with conservative estimates and adding up sales at the four largest U.S. carriers, approximately 13.1 million smartphones were sold during the quarter, of which 4.7 million, or 36%, were iPhones. Adding the impact from unlocked iPhones, and the share would be even higher. Remaining U.S. mobile carriers are too small to change the calculations one way or another.

iPhone Sales Were Down 16% in 3Q

iPhone 3Q sales trends are even more striking when considering total iPhone sales were down 16% sequentially during the quarter (I estimate the U.S. market saw a steeper decline of 20%+). iPhone sales were 17.1 million during 3Q, compared to 20.3 million in 2Q and 18.9 million in 1Q. Many consumers held off on smartphone purchases, or upgrades, since rumors of an updated iPhone were in the marketplace for a number of weeks (if not months).

Total iPhone Market Share

Nielsen’s market share data appears to show share of current smartphone usage, which I think is faulty and error-prone (one could make the argument that Nielsen is in fact just looking at 3Q sales data, however my previous calculations would prove otherwise). How does one measure how many phones are currently in use? Is Nielsen adding all of its prior quarterly shipment data to reach current market share usage? Such a method would lead to inconclusive data as it is unclear how many phones are still in use or have since been discarded. As an example, I bought an iPhone 3GS in 2009 and it has since been discarded to a pseudo iPod Touch. Since it is tough to estimate iPhone’s current overall usage share, one could instead look at big picture themes. According to Nielsen, iPhone has 28% share and it is reasonable to assume that iPhone’s share has improved with iPhone at Verizon. Is it possible that iPhone had less than 28% U.S. smartphone usage share in 2010 when iPhone accounted for over 60% of AT&T smartphone sales? I have my doubts.

What Is Going On?

My primary theory for why Nielsen’s market share data is wrong, or at least misleading, is that some OEMs have altered Android to such a degree that many “Android-powered” phones are actually better classified as feature phones - great for text messaging, but lacking mobile browsers or apps. Nielsen is then unable to distinguish Android-powered feature phones from smartphones and simply assumes any Android-powered phone must be a smartphone. Alternatively, AT&T and Verizon data is pretty straight forward with no confusion between feature phones and smartphones. I don’t think the shipped vs. sold argument is as relevant for mobile phones because the sales numbers being thrown around are much higher than that of the much smaller tablet market.

Looking Ahead

iPhone 4S sales are off to a fast start. Upcoming sales data points that I will be looking for will come from Apple, AT&T, Verizon, and Sprint. Until Nielsen, and other market survey companies, reveal where they are getting their data and how it is being calculated, I don’t think it should be relied on for investment or app development decisions.

Dissecting an Apple Bear

From my AAPL 4Q11 recap posted last night:

"Earnings misses are not the end of the world. They can be healthy, serving as a foundation for further gains. Misses act as a reset for increasingly lofty expectations. Problems arise though when people look for answers to an earnings miss and are quick to make incorrect assumptions…. Apple bears are getting louder. People are wondering. People are asking.”

It wasn’t too hard to find an Apple bear (or a “trader” with provocative thought questions as they often want to be thought of) with a good list of questions for AAPL shareholders. Today it’s courtesy of Doug Kass writing for the Street. I think his questions are a good summary of the main bearish arguments that are being floated against Apple.

(my comments in bold).

Kass: If I were an Apple shareholder, I would be asking myself the following eight questions this morning (I don’t have the answers, and I didn’t have the foresight to buy the shares at lower levels!):

- Valuation is rarely a market catalyst. Who doesn’t know that Apple’s valuation, excluding its cash position, appears inexpensive?

Since when was Apple’s valuation looked at as a catalyst for the shares? I actually have Apple’s P/E multiple declining through 2013. If you ask me; iPhone, iPad, iOS, and Apple management & culture isn’t too shabby of a catalyst list.

- In reading the analysts’ earnings post mortem and explanation of why the company missed on the bottom line, why is it only now so obvious to analysts that Apple has been impacted by iPhone purchase deferrals ahead of the introduction of the iPhone 4S? Why wasn’t that included in analysts’ estimates?

My post from last night pretty much answers this question. We still don’t know how people buy phones.

- In my few decades of investing experience, when companies cite the impact of weather, seasonality or product transitions (as was the case with Apple) as reasons for a profit miss, it is usually a sign of a company’s maturing (sales and earnings) growth cycle. Have we seen a peak in growth rates at Apple, and beyond the quarter catch-up, might we begin to see decelerating growth at Apple in 2012-2014?

If Apple actually missed its guidance, this question would make a lot more sense.

- Size matters. Should investors be surprised that, with annual revenue having risen (fiscal 2011 September year just completed) to over $108 billion, sales and profit growth will become more difficult going forward? Fiscal 2014 sales are projected to approach $200 billion. Have the outlook and expectations for Apple grown too optimistic?

Is he suggesting to buy smaller companies with weaker fundamentals because they have a smaller market capitalization?

- A 3 million unit shortfall in iPhone sales and slightly weaker iPad numbers (11.1 million vs. consensus of 11.6 million, but there were estimates for 13 million units!) resulted in the profit miss. Are investors overestimating the short-term growth prospects for the overall tablet market? And what about the weakening trend in iPod unit sales (down 27% year over year) that signal a secular decline in the product category? Doesn’t this place more pressure on the success of future new products?

His iPad question, addressed in my piece last night, contains some validity, however, its funny that these same people will then tout how other tablets - without an Apple logo - will do just fine. If the tablet market is not as big as initially thought (11 million iPads/quarter doesn’t seem too small to me), that doesn’t just spell trouble for Apple, it will mean Amazon, Google, and any other player looking to actually gain a footing in tablets will have a tough time.

- Apple’s corporate and product success are well known. Are these success too well known as manifested in a near unanimity of bullishness on the part of Wall Street’s sell side?

Is he suggesting to buy a company with more corporate and product failures because less people will be bullish on the stock?

- The ownership of Apple shares is broad, and institutional sentiment toward the company appears to be approaching a positive extreme. One could argue that the long side in Apple is crowded. Doesn’t everyone own the stock? Who will be the next investor in Apple’s shares that will catapult the valuation and shares toward the next and higher level)?

I thought everyone who wanted to own Apple already owned shares back at $250? Institutional owners aren’t allowed to add to their positions?

- Most recognize that Steve Jobs has already thought about and has contributed to another few years of new product innovation. But will the miss last night revive the issue whether the remarkable disruptive innovation instituted by Jobs (in the past) can be continued into the future after his imprint is removed?

Would this question have been asked if analysts’ expectations weren’t high and Apple instead blew consensus numbers out of the park?

Doug Kass did a good job at asking the obvious bearish questions, from a traders’ perspective. There is a bear argument to be made for every company (including Apple), but Kass’s arguments are largely irrelevant, focused on short-term stock movements. The actual long-term Apple bear argument centers around the scenario where Apple products become stale (see RIMM) and people begin to move away from iOS, iPhones and iPads. Additional Apple problems would center around conflict within Apple’s management team post Steve Jobs or post Tim Cook.

The best part about this post is I am only writing it - answering these bearish AAPL questions - because Apple is executing on all cylinders.

Final Thoughts on Apple's 4Q11

iPhone. We Still Don’t Know How People Buy Phones.

While everyone has been quick to blame unrealistic expectations for Apple’s 4Q11 “miss”, I think the rare earnings disappointment was partially due to a lack of understanding on how iPhone demand fluctuates and how people buy phones. Apple just became a much harder company to model.

It is incorrect to say that analysts never considered people waiting to buy iPhones ahead of a rumored iPhone refresh. Almost every analyst note published in the past three months mentioned an iPhone refresh and the tendency for pent-up demand to build as consumers wait on iPhone purchases. Apple management forewarned the same scenario on Apple’s 3Q11 earnings call. People were expecting it. Even my analysis was based on the idea that a slowdown in iPhone 4 sales in countries that typically get the new iPhone on launch would be offset by continued strong iPhone 4 sales in countries where the new iPhone would take months to reach. That didn’t happen.

Instead, the world pretty much stopped buying iPhones in September. I don’t think it’s much of an exaggeration to say that iPhone sales almost came to a screeching halt towards the end of September. Apple specifically mentioned that sales slowed further in the second half of the quarter. Running rough calculations, I estimate iPhone sales may have been tracking down 20-40% yoy in the U.S. towards the end of September. Pretty remarkable. I wonder if Apple retail stores saw this noticeable decline in demand? Analysts underestimated how many people were aware of iPhone rumors and were waiting to buy. Apple was surprised too, with both Tim Cook and Peter Oppenheimer mentioning “rumors” as one cause for weak iPhone sales. Anecdotally, I talked with quite a few BlackBerry and Android users over the summer, all of whom were well aware of a new iPhone coming out sometime in the fall. I assumed there were other people still buying iPhones.

The iPhone miss (and let me be clear, the iPhone number was pretty negative at only 21% yoy growth) came as a huge surprise with analysts and the investment community thinking the iPhone demand cycle had become independent of product transitions. We thought that sequential quarterly iPhone growth is the new normal, regardless of how a new iPhone impacts deferred sales. Apple’s significant 3Q11 iPhone beat cemented the idea of sequential quarterly growth. Ironically, many analysts thought the new iPhone was going to be unveiled at WWDC and had modeled for declining iPhone sales in 3Q11 due to deferred sales (people waiting). Instead, Apple beat everyone’s iPhone estimate by a mile as iPhone rumors really didn’t grow until August. Independent Apple analysts (including myself) concluded it would be unlikely that Apple would report a sequential quarterly decline in iPhone shipments in 4Q, which meant Apple would sell more than 20.3 million iPhones (their 3Q11 total). We weren’t necessary making a call on growth assumptions, or at least I wasn’t. Some analysts did get it right. Goldman Sachs modeled 16.9 million iPhones – essentially spot on. Still wondering why Goldman was picked first for Apple’s earnings Q&A?

I don’t think our iPhone expectations were overly optimistic though as our previous demand forecasts have now shifted to 1Q12. Our annual iPhone sales estimates remain largely unchanged. Instead, our timing was wrong. I think iPhone’s increasing demand complexity was the main culprit for the iPhone miss. Even Apple management thought they would sell more iPhones in 4Q11.* We still don’t understand how consumers buy phones. For many, buying a phone is categorized as “the big purchase” even though the actual cost of the phone is spread over 2 years. A $110 monthly cell phone bill 17 months from now is not as important as the difference between a free subsidized phone and a $199 subsidized phone today. People wait to buy phones until their contract is up and - this is key - they are willing to wait after their contract is up to take advantage of the carrier’s subsidy and buy a phone that they really want, even if it means holding off on a new cellphone for an extra 4 or 5 months. This trend will only grow as smart phones flourish.

Reports of record iPhone 4 sales over opening weekend (including positive commentary from AT&T, Verizon, and Sprint) are evidence that iPhone demand is back. Going forward, analysts should model a slowdown in iPhone sales during product transitions. If a new iPhone is rumored for October 2012, one should assume people will stop buying iPhones in September. Seems obvious now, but many got it wrong. In addition, a new form factor will also lead to difficultly in meeting initial supply, which could hurt early sales.

iPad. The Wild West.

Apple sold 11.1 million iPads in 4Q11. I expected 11.7 million and I had originally expected 11.1 million, so iPad is performing near my expectations. Unfortunately, many independent analysts have been running with extremely aggressive iPad expectations. I do think these expectations need to come down. Apple noted iPad supply and demand is now in balance. Apple sold every iPad that consumers desired; 11.1 million/quarter. I still get nervous with iPad because it is such a young product. What if demand really isn’t as good as we think? It doesn’t mean the product is a failure, instead maybe people just haven’t yet become comfortable with tablet computing. Sales fluctuations will occur and people need to plan for it. I found it interesting that Tim Cook made the claim that iPad could turn out to be larger than the PC market. In the past, Apple’s remarks were more vague and general. Apple wants to set the tone for iPad. This is the bet. This is the future.

Mac. Steady as She Goes.

Apple’s forgotten child (at least in many investor’s eyes) continues to do well, taking market share from Windows with both hands. Strong 37% yoy growth in portables (thank you Macbook Air) speaks well of Apple’s growing brand in the traditional PC market. Yet compared to iPad and iPhone, Mac’s influence is just too small to impact earnings to any large degree.

iPod. Out to Pasture.

Declining iPod sales are now normal and to be expected. In fact, iPod declines are accelerating. Sure, the “newer” iPods might change this trend a bit in the near term, but when excluding iPod Touch, the iPod is only a fraction of its former self.

Guidance. Strong.

Apple’s 1Q12 guidance was very strong, near current consensus (which is very rare). Management indicated they will sell a record number of iPhones and iPads during the holiday quarter (not that shocking). Since Apple “missed” earnings, analysts will be more conservative with their forward expectations, unsure of how much cushion Apple built into its guidance. Many analysts were already running with conservative assumptions so the 4Q11 “miss” should not weigh much on forward EPS estimates.

Thoughts on Apple. Quarterly Results Rarely Matter For Superior Management Teams

Earnings misses are not the end of the world. They can be healthy, serving as a foundation for further gains. Misses act as a reset for increasingly lofty expectations. Problems arise though when people look for answers to an earnings miss and are quick to make incorrect assumptions. A prime example is Apple’s retail store trends. Same store sales were down approximately 10% (which means that your local Apple store reported 10% less revenue, on average, this past quarter vs. last year – a pretty sizable decline). Well, hello, iPhone sales were miserable. With an ASP of over $600 and a concentration of Apple retail stores in the U.S., a slowdown in iPhone sales (maybe as much as 30-40% in September in the U.S.) will have an impact on total retail store revenue. It doesn’t take a genius to figure that out.

Apple will get penalized in the near-term because of its earnings “miss”. People will remain more cautious on iPhone and iPad growth. Expectations are being reduced (especially among the independents). Apple bears are getting louder. People are wondering. People are asking. Earlier this week, the biggest question was how high the stock would gap up after earnings. Now people are thinking of the “what ifs”, what if people stop buying iPhones, what if iPad sales slow down. While such questions might seem silly to think given the technicalities of Apple’s “miss”, its nevertheless happening.

Good companies sometimes have “bad” earnings reports (who would have thought 50% EPS growth would be considered bad). In such circumstances, time is your friend. For long-term investors, quarterly results shouldn’t even matter much, instead attention should be given to the current management team and its ability to innovate.

*UPDATE: Thanks to @adamthompson32 for pointing out that Apple actually said 4Q11 iPhone sales were better than expected. Tim Cook: “And as we have predicted…(iPhone) sell-through decline did occur in the quarter, but not nearly to the extent that we thought and therefore, we significantly beat our guidance.”

My Idol, Steve

Steve was one my idols, not because he helped build Apple Inc., but rather for his ability to turn Apple into a set of beliefs.

That technology is too powerful of a force to enjoy without acquired perception and natural intelligence.

That product design has the power to momentarily satisfy the never-ending search for order and reason.

Many are asking themselves why they feel so much sadness over Steve’s death even though they never knew him on a personal level. Steve became a symbol for many of us, representing how technology can push society forward. Edison advanced society in the late 19th and early 20th century, Disney in the early and mid-20th century, and Steve in the late 20th and early 21st century. Many tears are being shed over Steve’s death because deep down we know it’s unlikely we will see another visionary like Steve in our lifetime.

AAPL 4Q11 Earnings Cheat Sheet

AAPL Orchard Estimates (change from previous estimate in italics)

Revenue: $32.6 billion (up $600 million) (guidance: $25.0 billion/consensus: $29.0 billion)

GM: 40.5% (down 40 basis points) (guidance: 38.0%/consensus 39.6%).

EPS: $8.55 (up $0.10) (guidance: $5.50/consensus: $7.16).

Product Unit Sales Estimates

Macs: 4.8 million (up 100,000)

iPad: 11.8 million (up 700,000)

iPod: 7.2 million (unchanged)

iPhone: 23.3 million (unchanged)

I remain confident in my initial quarterly estimates, published July 26, making only modest tweaks to a few variables. I raised my iPad sales estimate 700,000 units to reflect a higher production yield. I am maintaining my iPhone sales estimate (which I initially thought was too high) as the iPhone 4S is pushed out to 1Q12 and iPhone 4 supply draw-down did not occur to any major extent in 4Q.

Things to look for:

iPad Sales. Apple may provide an iPad sales update at next week’s iPhone event. Apple was successful in increasing iPad production in 3Q11 and many will look for continued gains in 4Q11. While my estimate calls for 11.8 million iPads, Street consensus may actually be slightly higher. I think iPad sales greater than 10 million will be deemed okay by the Street, while more than 13 million iPads will be considered strong.

iPhone Sales. With the iPhone 4S launch pushed out to 1Q12, I don’t think we will see too much of a drop-off in iPhone 4 demand, especially considering iPhone 4 was recently brought to new carriers and countries. Apple may still get a pass if iPhone sales are on the weak side as analysts will simply blame iPhone 4S ramifications such as pent-up demand. iPhone sales greater than 20 million will be deemed good, while more than 25 million will be considered strong. iPhone 4S launch weekend sales figures may also be shared on the call (although it is just as possible that the iPhone launch will occur after October 18 or Apple will choose to not disclose initial sales).

Guidance. Similar to previous quarters, investors will look for Apple’s 1Q12 guidance for evidence of any economic impact or weaker iPad/iPhone production plans. Unfortunately, management’s conservative nature will make it very difficult to reach solid conclusions. My initial 1Q12 EPS estimate is $10.00 (Street consensus is $8.83) on $39.7 billion of revenue. I would consider EPS guidance around $7.00, with revenue in high $20s billion, as solid.

Two other scenarios may occur: 1) Apple may announce extra conservative EPS guidance due to economic concerns or 2) iPhone supply concerns related to the iPhone 4S launch. I think extra conservative EPS guidance would be something like $5.50, which compares to Apple’s reported $6.43 in 1Q11 (one could make the argument that Apple will put guidance at least above last year’s $6.43 EPS).

If Apple delivers a blow out 4Q11 quarter, chances are good Apple may run with extra conservative 1Q12 guidance as analysts won’t necessarily increase 1Q12 estimates, but would still maintain Apple target prices due to the 4Q11 beat. Accordingly, expectations wouldn’t be raised too high and Apple will be in a good position for another solid holiday quarter.

Thoughts on Facebook F8

1) Replacing the World Wide Web. Facebook is focused on replacing large swaths of the web. We got to see Facebook’s plan for sharing media, and I suspect we will hear Facebook’s take on other web functions, such as commerce, search, and utility, in the future.

2) Facebook Hates Privacy. Privacy remains Facebook’s major roadblock as web-replacement initiatives don’t look as appealing if Facebook users flock to high privacy safeguards. Although society has grown more comfortable with sharing information on the web; users’ ability and willingness to share will only strengthen Facebook’s intentions.

3) An Alternative. Facebook is presenting an alternative to Apple’s app model in terms of how users access and use third-party content. By no means is Facebook’s app model guaranteed to succeed, but it is clear that Apple’s native app model will have some form of competition. Apple has made an effort to point out the billions of dollars in app revenue returned to developers and I think Apple will reinforce this point, arguing app innovation should continue to flock to the iOS platform because developers actually get paid.

4) Changing Landscape. We are in the beginning stages of a changing tech landscape where the hardware battle will be won by economies of scale and uniformity, while the software battle is won by seamless integration between the social network and third-party content. Apple is in a prime position to reap competitive advantages from its manufacturing and supply chain economics of scale, while iPhone and iPad popularity may soon result in 100s of millions of iDevices in the wild. Meanwhile, I believe Facebook has already won the social network race and will now work on increasing and improving third-party content utilization. Apple and Facebook are in prime position to control the tech landscape.

Anchoring Bias Impacting Wall Street's View on Apple

Predicting tech trends beyond 6-12 months is somewhat of a futile endeavor, but two groups of analysts attempt the feat: paid and non-paid. Paid analysts largely encompass sell-side analysts - think along the lines of Goldman Sachs and Piper Jaffray. Non-paid analysts include everyone else and seem to have acquired the “independent” nomenclature. There remains another group - buy-side (think hedge funds and mutual funds) - who don’t actually publish Apple forecasts, instead utilizing paid (and independent) analysts forecasts.

Modeling Apple’s business (and earnings) involves two parts:

1) Knowing how to model a company’s financials. This is the easy part. Setting up an excel sheet to model revenues, expenses, and earnings going forward. Financial modeling is essentially Finance 101 (ironically many students have no clue what they are doing when they take intro Finance classes since the field is so disorganized academically in primary and high school).

2) Knowing how to model a company’s performance. This is the hard part. This is the part of modeling that is more art than science. How many iPads will Apple sell next year? How about iPhones? Experience, intelligence, and a clear mind separate the amateurs from the professionals.

I’ve discovered that looking at someone’s forward Apple projections reveals a lot about what they think of Apple and this is where things get interesting. Sell-side consensus for Apple earnings per share currently stands at $32.35 for fiscal year 2012 and $36.94 for fiscal year 2013. From a stock valuation standpoint, these numbers are important, but converting these numbers into growth, Wall Street believes Apple will grow 18% in 2012 and 14% in 2013.

In order to put these numbers in context, I compare Apple’s projected earnings growth to other technology companies:

2012 2013

GOOG: 19% 17%

IBM: 11% 11%

MSFT: 6% 9%

HPQ: -1% 2%

RIMM: -20% 2%

DELL: 26% -2%

Average: 7% 7%

AAPL: 18% 14%

(consensus data from FactSet and current as of 9/10/11)

Now we are getting a better picture of how Wall Street views Apple. Tim Cook and company are expected to outperform the overall technology sector, growing earnings 14% in 2013, versus a peer average of 7%. However, Apple’s 14% projected growth in 2013 pails in comparison to current 70% growth. What is going on here?

Instead of sell-side analysts “not getting it” - as some independent Apple analysts say, I think anchoring bias is the main culprit.

I thought Wikipedia did a good job at trying to define anchoring in a few sentences:

Anchoring and adjustment is a psychological heuristic that influences the way people intuitively assess probabilities. According to this heuristic, people start with an implicitly suggested reference point (the “anchor”) and make adjustments to it to reach their estimate. A person begins with a first approximation (anchor) and then makes incremental adjustments based on additional information.

Sell-side analysts are comparing Apple to its peers too much. Although analysts still believe Apple will outperform, many are modeling Apple with a 5-10% technology industry growth rate in mind. Apple’s growth is then pegged above this range, albeit by only a small margin. Apple is being anchored to its peers and corresponding lower growth rates.

Sell-side analysts may think Apple will sell a ton of iPhone and iPads, but end up with much lower Apple growth rates because Apple’s peers are performing so poorly. To make matters worse, much of this comparing, and anchoring, is occurring on a subconscious level, making it that much harder to acknowledge and correct.

Meanwhile, independent Apple analysts aren’t subjected to anchoring bias since they are only modeling Apple. In a way, they are able to put Apple in a valuation bubble. If independent analysts began to model Apple peers on a regular basis, I would suspect anchoring would become a bigger issue among the group.

As an independent Apple analyst, how fast do I think Apple will grow earnings?

2012: 40%+

2013: 35%+

My 2012 earnings growth estimate is twice the pace of Wall Street’s 18% growth estimate.

RIMM’s troubles, HPQ’s reorganization, MSFT’s status quo, and GOOG’s continuing mystery are causing Wall Street to view Apple with a more conservative eye. What is the solution? Unfortunately, I don’t expect Wall Street’s anchoring bias to end anytime soon. Apple will continue reporting large quarterly earnings beats, while Wall Street continues to gush over Apple’s growth.

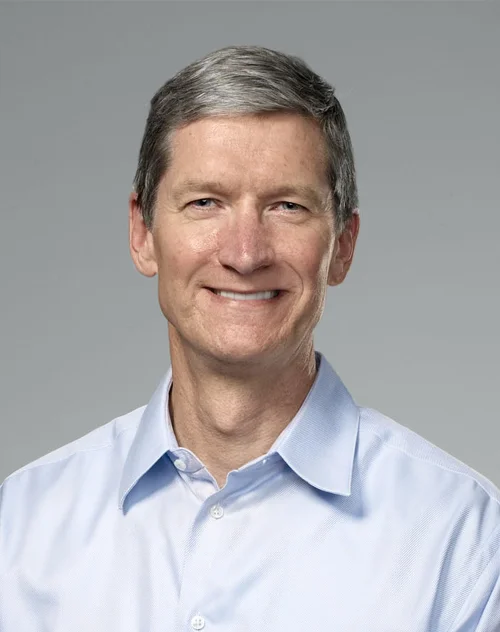

Tim Cook. The Architect.

While some have responded to Steve’s resignation as Apple CEO by recalling personal stories involving Steve or Apple, others have focused on how Apple’s culture will handle a different leader. Let’s take a step back and reassess Apple’s current situation.

Current Products

I have extreme confidence that Apple will successfully update its flagship products in the near-term. As I previously wrote, Apple’s start-up structure assures resources are allocated to a product in the months leading up to a refresh; breaking down the “walls” between executives and workers - the same walls that often destroy other technology companies. Having executives involved in seemingly detailed and mundane aspects of a product is the difference between having a product be “magical” or “good”. Tim Cook will continue to hash out aggressive business contracts with Apple friends and foes. Apple’s expanding supply and distribution channels will continue to be run with the dedication and intelligence that have put competitors to shame. As a prime example of how much confidence I have in Apple’s ability to execute in the near-term, I have no intention in lowering my forecasts for Mac, iPod, iPhone, or iPad sales in my AAPL earnings model following Steve’s resignation.

Future Products

Apple will continue to innovate and brainstorm ideas that will change the world. While it is difficult to pinpoint why the iPod, iPhone, and iPad have been so successful, it is important for Apple to continue to make similar industry-changing strides. I think this is where Apple will face its first significant challenge with Steve no longer at the helm. What makes Apple so great is its willingness to take abnormally large risks and essentially bet the farm on those risks. Apple is able to translate a big idea (big bet) into reality with very little friction and inefficiency. The biggest risk enters the equation on the demand side - whether consumers want the product. Steve made bets. Big ones. Will Tim be able, or willing, to take similar big risks?

At this time, I do think Tim is capable of such responsibility. Tim isn’t some young gun who has been thrown into the game. Observing how the world has changed (and where it will go) is an art not a science, and while Steve mastered that art so successfully, Tim was in a perfect position to watch the master perfect his art, giving him a significant advantage over everyone else in Silicon Valley. Apple will lose on some bets, but will still be able to strive to new heights if more is wagered on winning bets.

Face of Apple

Apple is Steve and Steve is Apple and that will not change. However, there is now a debate as to who will become the new face of Apple or if Apple even needs a singular public representative given Apple’s size and power. I do think the entire Apple executive team will gain more exposure with some SVPs acquiring new affiliations with consumers. Forstall as Mr. iPhone and iPad, Jony as Mr. Apple Design, Schiller as Mr. Apple Brand, while Tim remains the “Big Dad”. Great brands create emotional connections between users and products. People will want to connect with Apple and its leadership in new ways. When Apple is ready to unveil its next big thing, we will most likely have a few members of the Apple team explain why the world needs this new product, whereas up to now, only Steve has had the honor.

AAPL

Concerning financials and other AAPL stock decisions, I would expect no significant changes or speed bumps with Tim as CEO. In addition, an internal CEO promotion often results in minimal changes to prevailing capital philosophies concerning dividends and share buybacks.

The Architect

At the end of the day, Steve built the foundation for a magnificent castle and Tim is a great architect. As I wrote back in December: "As long as most of the risk variables are monitored and marginalized to a certain extent by upper management (and Steve Tim) - the consumer is left as the biggest risks. Apple can then rely on its brand power to turn the odds in its favor.”

Inflection Point: HP webOS

HP’s decision to discontinue webOS devices and look for strategic alternatives, including the outright sale of webOS, marks a significant inflection point for the mobile industry. The barriers of entry are now too high for a new mobile OS. For the next 5-10 years, iOS, Android, (and Windows) will shape the future of mobile.

While there are still questions as to what value is left in webOS and rather patents/IP may still be of interest to potential bidders, the era of being able to grow an integrated ecosystem from scratch is over.

AAPL Orchard's AAPL 4Q11 Estimate

Overall Quarter Metrics

I expect iPad and iPhone to represent nearly 70% of Apple’s quarterly revenue. Remarkable.

Apple’s margin in 2011 has ranged from 38.5% to 41.7%. Management explained the 41.7% margin experienced in 3Q11 included some one-time warranty benefits and guidance of 38% for 4Q11 is primarily driven by the product mix. I don’t buy it. I don’t see many reasons for Apple’s margin to set a new low for 2011 in 4Q due to more iPhones (mostly iPhone 4 and 3GS) and iPads being sold. I expect attractive component pricing trends will offset any modest impact from back-to-school promotions (Macs and certain iPods are discounted). Timing issues surrounding the next iPhone may very well push margin pressure out to 1Q12. I would expect more bullish estimates to have GM closer to 41.5%.

I expect Apple to report 82% yoy earnings growth. While 82% growth is down from 122% yoy growth seen in 3Q11, I would not make much of this decline. Most of the difference is related to the ramp up in iPhone unit sales in 2010.

Product Unit Sales and Commentary

I expect MacBook Air and Mac mini updates to contribute to another solid Mac quarter. Apple will continue to take market share from Windows (early stages of 5-10+ year trend). As the PC market struggles to grow (thanks in part to the proliferation of smartphones and iPad), I view Mac growth greater than a range of 10%-15% as very respectable.

With iPad supply/demand still out of balance in a number of countries, I expect Apple to continue to expand the iPad channel during the quarter. While it remains to be seen if back-to-school purchases will include iPad, I don’t see many hiccups to stellar iPad demand during 4Q. Rumors of a possible iPad Pro have been very sporadic and I don’t expect such rumors to impact mainstream consumer purchasing habits. As seen with 3Q iPad growth of 183%, Apple has expanded iPad production nicely and is capable of greater than 100% year-over-year unit shipment growth.

I expect strong iPod touch sales to be offset by the continued decline in Apple’s other iPod models. Going by historical trends, Apple will refresh the iPod line up near the end of 4Q11, possibly at the same time as the expected iPhone refresh. I would not necessarily expect a large move in iPod shipments one way or another because of this refresh event, unless Apple moves forward with a plan for a low cost iPhone that includes changes to the iPod touch.

I expect Apple to unveil the new iPhone in September. Traditionally, I would include a significant supply drawdown of the old iPhone model, followed by a slow ramp up of the new iPhone model to go along with an iPhone refresh, but last quarter’s amazing iPhone sales lead me to believe Apple will continue to post sequential quarterly iPhone unit growth. I expect Apple will continue to sell iPhone 4 (and possibly iPhone 3GS) into 2012, therefore I am not expecting a significant drawdown in iPhone shipments in the weeks leading up to the iPhone refresh as iPhone 4 roll-out continues to new carriers and countries. Additionally, I would expect pent-up iPhone (4s or 5) demand will continue to grow during the quarter. Similar to the iPad 2 supply debacle, I expect the next iPhone to experience the same craziness and supply shortages in its first few months of sale, which will only help Apple’s 1Q12 iPhone numbers.

Similar to other sell-side analysts, I will most likely be revisiting my estimates following the end of the quarter. At this point, I would attribute any significant differences to my EPS estimate to differences in iPhone unit shipments. Questions can be addressed to me through twitter.

Apple CEO Succession 101

Daring Fireball’s thoughts on Apple’s CEO succession: click here.

My thoughts?

Issues like Apple CEO succession show how little people understand Apple.

This is Apple’s next CEO: Tim Cook

From Apple:

"Cook is responsible for all of the company’s worldwide sales and operations, including end-to-end management of Apple’s supply chain, sales activities, and service and support in all markets and countries. He also heads Apple’s Macintosh division and plays a key role in the continued development of strategic reseller and supplier relationships, ensuring flexibility in response to an increasingly demanding marketplace."

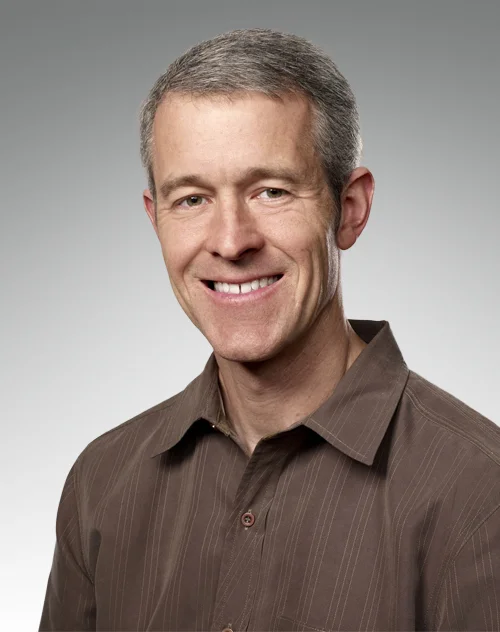

This is Apple’s backup CEO: Jeff Williams

From Apple:

"Jeff Williams is Apple’s senior vice president of Operations, reporting to COO Tim Cook. Jeff leads a team of people around the world responsible for end-to-end supply chain management and dedicated to ensuring that Apple products meet the highest standards of quality.

Jeff joined Apple in 1998 as head of worldwide procurement and in 2004 he was named vice president of Operations. In 2007, Jeff played a significant role in Apple’s entry into the mobile phone market with the launch of the iPhone, and he has led worldwide operations for iPod and iPhone since that time.”

I have my reasons supporting this Apple CEO succession hypothesis. Stay tuned to AAPL Orchard for more commentary on this issue in the future.

I publish a daily email about Apple called AAPL Orchard. Click here for more information and to subscribe.

Great Use for Apple's Cash

City Urban Core Population # of Apple Stores

Shanghai, China 9,495,701 2

Beijing, China 7,296,962 2

Hong Kong, China 6,780,000 0

Tianjin, China 5,066,129 0

Wuhan, China 4,488,892 0

Guangzhou, China 4,154,808 0

Shenyang, China 3,981,023 0

Chongqing, China 3,934,239 0

Nanjing, China 2,822,117 0

Fuzhou, China 2,710,000 0

Harbin, China 2,672,069 0

Xi’an, China 2,588,987 0

Chengdu, China 2,341,203 0

Changchun, China 2,223,170 0

Dalian, China 2,118,087 0

Hangzhou, China 1,932,612 0

Jinan, China 1,917,204 0

Taiyuan, China 1,905,403 0

Qingdao, China 1,867,365 0

Zhengzhou, China 1,688,681 0

Shijiazhuang, China 1,632,271 0

Kunming, China 1,549,593 0

Lanzhou, China 1,527,383 0

Zibo, China 1,514,070 0

Changsha, China 1,489,259 0

Nanchang, China 1,386,454 0

Urumqi, China 1,358,986 0

Guiyang, China 1,341,243 0

Anshan, China 1,287,136 0

Tangshan, China 1,279,226 0

Wuxi, China 1,245,129 0

Jilin City, China 1,244,725 0

Fushun, China 1,244,144 0

Suzhou, China 1,170,618 0

Baotou, China 1,146,506 0

Qiqihar, China 1,125,948 0

Xuzhou, China 1,120,534 0

Hefei, China 1,107,143 0

Handan, China 1,069,146 0

Shenzhen, China 1,058,531 0

Luoyang, China 1,043,243 0

Nanning, China 1,016,013 0

West Des Moines, Iowa 46,403 1

Newark, Delaware 28,547 1

Leawood, Kansas 27,656 1

Tukwila, Washington 17,392 1

Buford, Georgia 10,668 1

Emeryville, California 9,859 1

Apple expects to utilize $650 million for retail store facilities in 2011, opening 40 new stores worldwide, 70% to be located outside the U.S.

And people wonder what Apple will spend its cash on…

A New AAPL Era

Apple reported its most recent quarterly earnings this evening. Impressive would be an understatement.

Here are some talking points:

1) Emerging Market Growth. Skewed perspective is making it hard to understand how fast Apple is growing. Many tech analysts are situated in developed countries and economies where the Apple brand is well established, and accordingly have a harder time conceptualizing how Apple can maintain dramatic growth rates. The combination of rising standards of living and the increasing availability of lower-priced Apple products is a new trend for emerging markets, and it is reasonable to expect this scenario to drive Apple’s growth in the future.

2) Product Line Diversification. Similar to the iPod, we are seeing the emergence of the iPhone product line: a series of iPhones with a sliding scale of features and capabilities. By the end of 2011, iPhone 3GS, iPhone 4, and iPhone (4S or 5) will most likely round out Apple’s iPhone line. Importantly, each iPhone utilizes iOS apps and has access to the iTunes store. I see the same trend happening with the iPad in due time; multiple versions sold simultaneous at different price points. Apple will rely on this product line diversification to cater to different market segments using price as a key differentiator. Emerging markets will have iPhone 3GS, mainstream will be content with iPhone 4, and early adopters will go crazy over iPhone (4s or 5). In addition, Apple’s overall margin benefits from the continued sale of “older” products as component pricing generally declines over time.

3) Big Losers and Winners. Apple management was very clear on the earnings conference call: iPads are eating away at Windows PC sales and iPhone continues to grow like a wild weed. Companies focused on selling consumer hardware (Dell, HP, RIMM, Motorola, and Samsung) are in a very difficult position as each is starting to understand that having good software is just as important as selling sexy hardware. Big winners (besides Apple) include companies who luckily aren’t competing in the consumer market, and are instead focusing on selling enterprise services or infrastructure needed to foster commerce and further innovation (IBM and Oracle come to mind). It is no coincidence that Dell, HP, RIMM, Motorola, and Samsung have indicated (or will indicate) an interest in entering the enterprise services market.

Random Bytes:

-) Look for Android activation numbers to become less relevant as time goes on. I have this growing feeling that Google is nervous that Android is becoming nothing more than a large void, taking up mobile space, and is relying on activation numbers to impress app developers to dedicate resources to the platform. It’s not working. iOS reached critical mass a few quarters ago and Android will not stop iOS momentum.

-) While I will keep AAPL stock thoughts to myself (at this time), it is important to remember that the large institutional holders control Apple stock and many of these entities are not interested in quick 5-10% stock moves, but instead the attractiveness of AAPL 5-10 years out. Potential AAPL dividend payout ratios, cash flows, and cash holdings will begin to matter just as much as iOS market share, iOS user statistics, or other random Apple product data points. The big boys will continue to support AAPL as long as they feel confident they will receive an annual return that beats other asset classes (fixed income, real estate, etc.) over an extended period of time.