Making the Case for Doubling Apple's Share Buyback Pace

Next week, Apple will provide an update to its capital return program. In what has become an annual tradition, the announcement will include a sizable increase to Apple's share repurchase authorization and a hike in the quarterly cash dividend. Given recent management commentary, Apple's overall thought process regarding capital allocation is already known. The only way Apple will be able to accomplish its capital return goals is by doubling the pace of share buyback from current levels.

Capital Return Update

For the past five years, Apple has used FY2Q earnings to announce updates to its capital return program. Here are the changes Apple announced to its share buyback authorization over the years:

2012: $10 billion buyback authorization

2013: $60 billion (increase of $50 billion)

2014: $90 billion (increase of $30 billion)

2015: $140 billion (increase of $50 billion)

2016: $175 billion (increase of $35 billion)

2017: $210 billion (increase of $35 billion)

In terms of the quarterly cash dividend, Apple has announced five increases over the years:

2012: $0.38 per share

2013: $0.44 (15% increase)

2014: $0.47 (8% increase)

2015: $0.52 (11% increase)

2016: $0.57 (10% increase)

2017: $0.63 (11% increase)

Excess Cash

In order to assess the most likely changes Apple will announce next week to its share buyback authorization and quarterly cash dividend strategy, we turn to recent comments from Apple CFO Luca Maestri:

"Tax reform will allow us to pursue a more optimal capital structure for our company. Our current net cash position is $163 billion. And given the increased financial and operational flexibility from the access to our foreign cash, we are targeting to become approximately net cash neutral over time."

Maestri's comments tell us three things:

Apple considers its current excess cash position to be $163 billion. After taking into account repatriation taxes, Apple's excess cash totals approximately $125 billion.

Apple wants to remove the vast majority of this excess cash from the balance sheet in order to reach "a more optimal capital structure." This isn't a management team that will sit on the excess cash indefinitely.

Apple's "net cash neutral" target implies management is okay with holding debt on the balance sheet. It's not likely that Apple will use excess cash to reduce its debt obligations significantly.

In addition to holding $125 billion of excess cash (after taxes), Apple is also kicking off significant amounts of cash. A successful capital return strategy needs to account for this ongoing cash flow generation. The company is currently generating approximately $50 billion of free cash flow per year. This total reflects approximately $60 billion of operating cash flow per year and between $10 billion and $15 billion spent on property, plant, & equipment. Over the next five years, it is conceivable that Apple will generate more than $200 billion of free cash flow. Management has been funneling nearly all of its free cash flow into capital return initiatives.

Combining Apple's $125 billion of excess cash currently on the balance sheet with its $200 billion of free cash flow generation, Apple is on track to have $325 billion of excess cash over the next five years. Without record-breaking increases to share buyback authorization and quarterly cash dividends, Apple will have trouble spending this excess cash prudently in a timely manner. Since 2012, Apple has spent just shy of $250 billion on capital return initiatives. Assuming Apple maintains its current share buyback pace and cash dividend payouts, it would take Apple close to ten years to spend $325 billion of excess cash. Big changes are needed in order for Apple to reach an optimal capital strategy in a reasonable amount of time.

Changes

Apple has a number of options at its disposal when it comes to spending $325 billion of excess cash over the next five years. The company can utilize mechanisms like a Dutch auction tender offer to repurchase a significant number of shares in a very short amount of time. There are also various cash dividend strategies that management can follow involving special dividends. However, the odds of Apple utilizing such strategies are not high. Instead, Apple will likely follow its existing capital return strategy but at much higher levels. Such a strategy is realistic, achievable, and financially prudent for shareholders.

One possible path Apple can follow includes announcing the following changes next week:

Increase share buyback authorization by $100 billion (would represent a record increase).

Increase the quarterly cash dividend by 20% to $0.75 per share (would represent a record increase).

Buyback Changes

Apple is currently buying back approximately $30 billion of shares per year. While this is a significant amount for any company to spend on share repurchases, Apple will have to materially increase this buyback pace to spend its excess cash in a timely manner. At the same time, there are limits as to the number of shares Apple can realistically buy back before distorting the market. (My Apple stock buyback program primer is available for Above Avalon subscribers here.)

Increasing share buyback authorization by $100 billion would give Apple the best of both worlds: the ability to buy back substantially more shares over the next two years while avoiding much market dislocation. In fact, a $100 billion authorization would allow Apple to double its buyback pace to $60 billion per year. Given Apple's daily trading volume, a $60 billion annual share buyback pace amounts to about 10 days of AAPL buying pressure. In subsequent years, Apple could announce smaller increases to buyback authorization in the range of $50 billion to $75 billion. This would be done to maintain the $60 billion per year buyback pace.

As shown in Exhibit 1, Apple can continue to utilize both open market transactions and accelerated share repurchase arrangements (ASRs) to buy back shares. The ramp in buyback from 2017 to 2020 reflects the amount of time Apple will utilize to bring back foreign cash to U.S. subsidiaries.

Exhibit 1: Apple Share Buyback

In the above scenario, Apple will have spent $275 billion on share buyback over the next five years. While Apple could certainly announce a larger increase to share buyback authorization next week such as $125 billion or even $150 billion, it's not likely that such authorization would result in a significantly higher buyback pace as Apple must still back its foreign cash to U.S. subsidiaries. In addition, a significant higher pace of share buyback would begin to raise questions about market dislocation.

Dividend Changes

A scenario that includes doubling its share buyback pace will have a major impact on Apple's dividend strategy. The company has been following a dividend strategy of conservative year-over-year increases in dividend expense. Due to the share buyback program, Apple has been able to grow dividends per share by larger margins each year given the reduction in the number of shares outstanding. Whereas Apple's dividend expense has increased by 21% since 2013, Apple's quarterly cash dividend has increased 66% during the same time period.

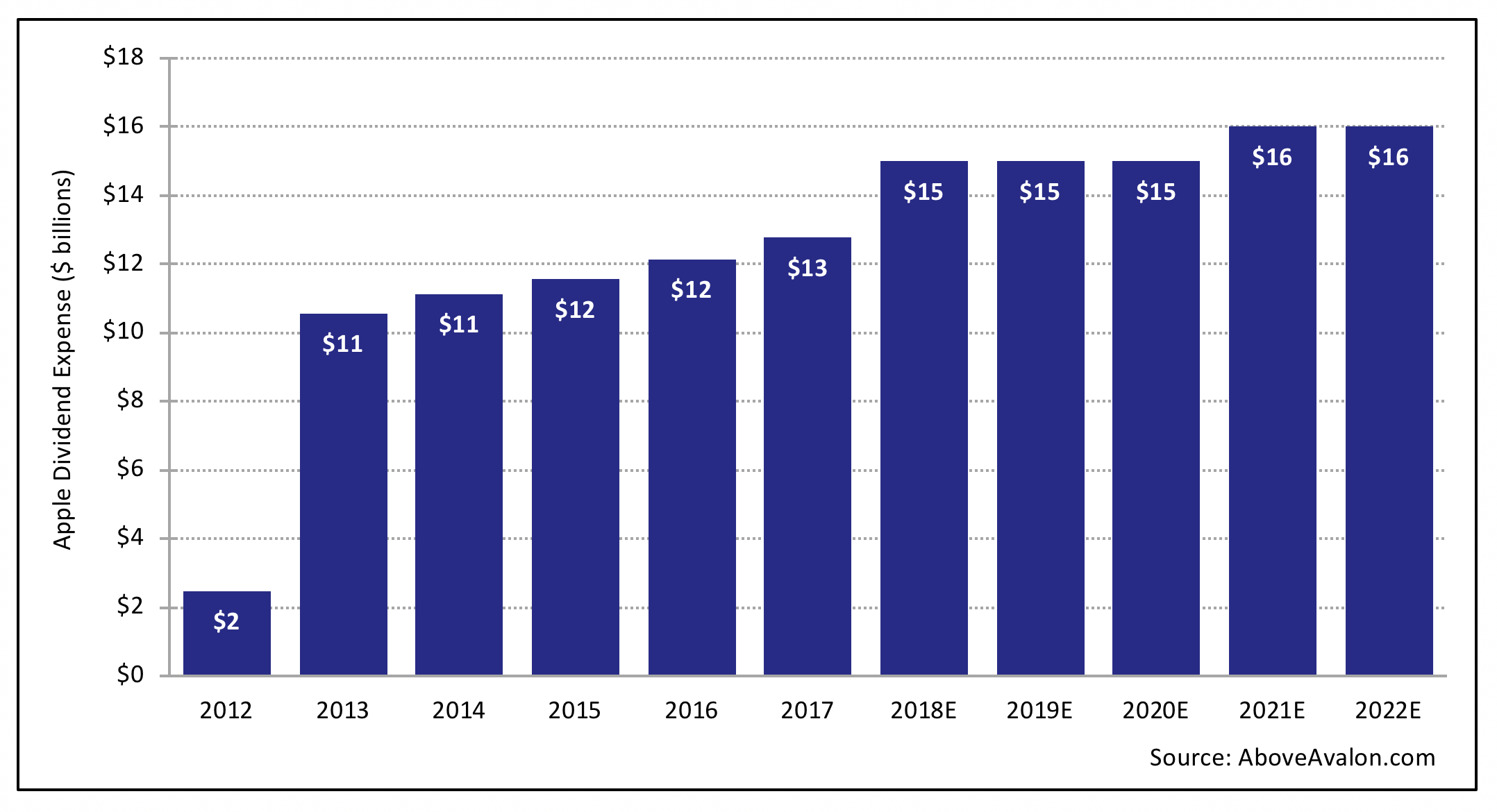

By ramping share buyback to $60 billion per year and increasing dividend expense gradually to $16 billion per year in 2021 (from the current $13 billion a year), as shown in Exhibit 2, it is possible for Apple to increase its quarterly cash dividend per share by as much as 80% over the next five years. In this scenario, Apple's dividend expense would increase by only 25% during the same time period.

Exhibit 2: Apple Dividend Expense

In the above scenario, Apple will have spent close to $75 billion on dividend expense over the next five years. The exact magnitude of Apple's dividend increase will be dependent on the price at which the company buys back its shares in the coming years. However, there is no question that Apple's quarterly cash dividend stands to benefit from a large increase in share buyback pace. An 80% increase over five years would bring Apple's quarterly cash dividend to $1.10 per share by the end of 2022.

Summary

Apple's balance sheet objective is to reach an optimal capital structure by giving excess cash back to shareholders. This goal will be achieved via the continued use of share repurchases and quarterly cash dividends. Following U.S. corporate tax reform, and assuming continued robust free cash flow generation, Apple will possess as much as $325 billion of excess cash over the next five years.

As shown in Exhibit 3, a realistic and prudent way for Apple to remove this excess cash from the balance sheet is to double the pace of share buyback (from $30 billion to $60 billion) while gradually increasing the amount spent on dividend expense over time.

Exhibit 3: Apple's Capital Return Program

By spending $75 billion per year on capital return initiatives, up from the current $45 billion per year pace, Apple will be on track to spend more than $325 billion of excess cash in order to reach an optimal capital structure.

Receive my analysis and perspective on Apple throughout the week via exclusive daily updates (2-3 stories per day, 10-12 stories per week). Available to Above Avalon members. To sign up and for more information on membership, visit the membership page.