Apple 2Q18 Earnings Expectations

Wall Street has major jitters when it comes to Apple's upcoming earnings release. Sentiment has decidedly swung toward the negative as questions swirl around iPhone X demand. Despite the dramatic downturn in expectations, Apple's stock price has held up remarkably well. While many eyes will be on iPhone sales tomorrow, my suspicion is that the data point won't have as much influence as consensus assumes. Instead, Apple's capital return update has the potential to be the major takeaway from 2Q18 earnings.

The following table contains my Apple 2Q18 estimates. The ingredients are in place for Apple to report a slight EPS beat to consensus although 3Q18 revenue guidance will likely come in below consensus.

My full perspective and commentary behind these estimates are available to Above Avalon subscribers. (Become a subscriber to access my full 5,000-word Apple 2Q18 earnings preview available here. To sign up, visit the subscription page.)

Items Worth Watching

Here are the five variables worth watching when Apple releases earnings on Tuesday:

iPhone Channel Inventory. Given prior management commentary, iPhone unit sell-through growth and iPhone average selling price don't represent the major wildcards for 2Q18 earnings. Instead, the big unknown is found with iPhone channel inventory. A significant channel inventory drawdown will result in Apple reporting iPhone unit sales closer to 50M units. Vice versa, a relatively minor decline in iPhone channel inventory may lead to Apple reporting iPhone sales slightly ahead of my 52M unit expectation.

iPad ASP. The days of dramatic iPad unit sales declines are over. Accordingly, instead of unit sales, average selling price (ASP) stands to provide much more information regarding the latest iPad trends. A weaker-than-expected iPad ASP may support the view that the 9.7-inch iPad at the low end of the line is likely gaining momentum at the expense of the higher-end iPad Pro options.

Other Products. Apple's "Other Products" category has the sales momentum. The line item includes various products such as Apple Watch, AirPods, HomePod, Beats headphones, iPod touch, and Apple-branded and third-party accessories.

3Q18 Guidance. Apple's 3Q18 revenue guidance will likely provide a few clues as to how iPhone demand has been trending. One complicating factor when it comes to revenue guidance is that Apple's non-iPhone part of the business is seeing major momentum. iPhone weakness will be partially offset by strength in Other Products and Services.

Capital Return. Apple will announce changes to its capital return program. My expectations are for a $100 billion increase to share buyback authorization and a 20% increase to the quarterly cash dividend. Management commentary regarding timing associated with share repurchases will be closely monitored.

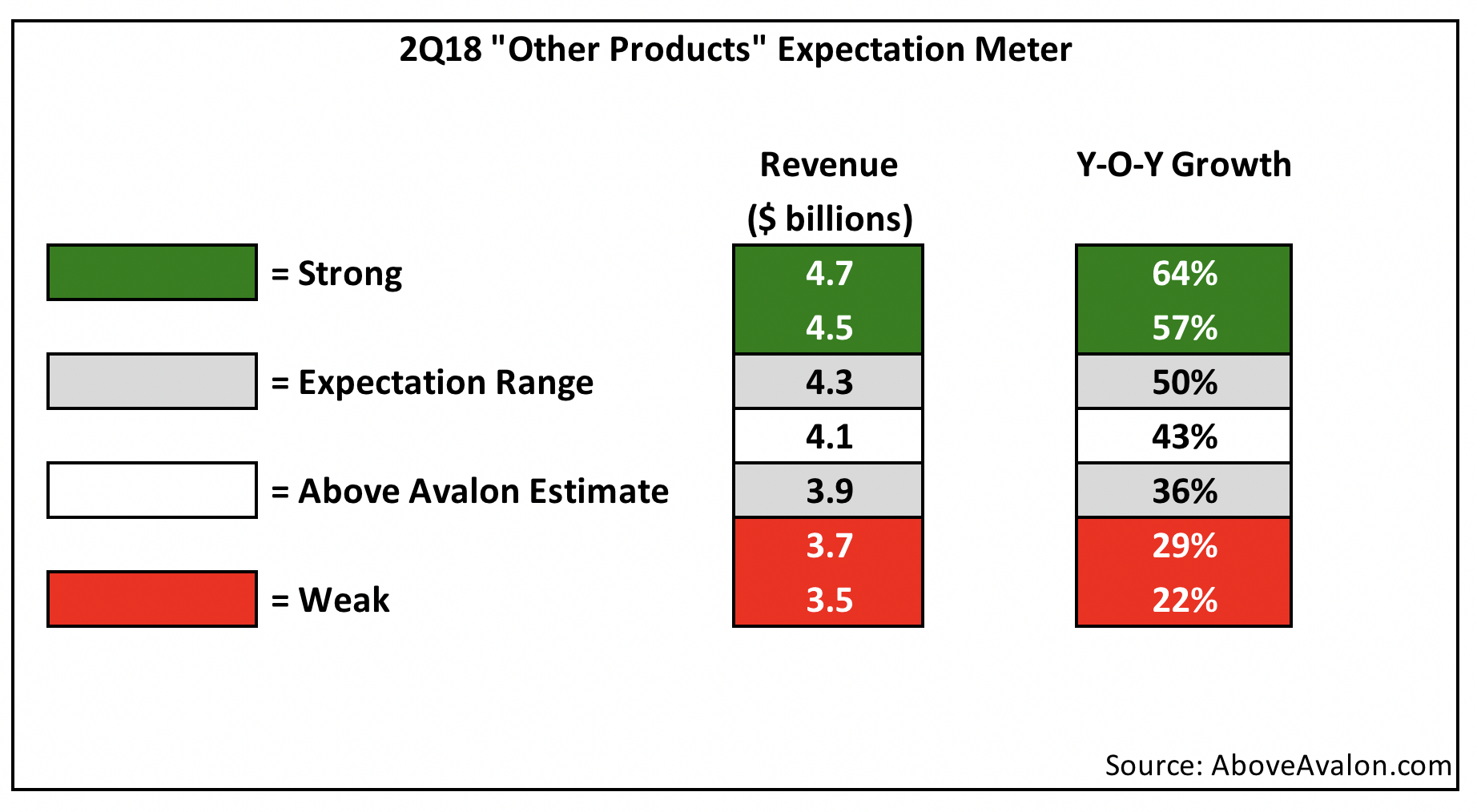

2Q18 Expectation Meters

Each quarter, I publish expectation meters ahead of Apple's earnings release. Expectation meters turn single-point financial estimates into more useful ranges that aid in judging Apple's quarterly performance.

In each expectation meter, the grey shaded area is my expectation range. A result that falls within this range signifies that the product or variable being measured is performing as expected. A result in the green shaded area denotes strong performance and likely leads me to raise my assumptions and estimates going forward. Vice-versa, a result in the red shaded area has the opposite effect and leads me to reduce my assumptions.

I am publishing three expectations meters this quarter: iPhone unit sales, Other Products, and 3Q18 guidance.

My iPhone unit sales expectation range stretches from 50M to 54M iPhones. iPhone unit sales within this range would be labeled as expected. If Apple reports iPhone sales greater than 54M units, results would best be described as strong. A sub-50M iPhone result would lead me to reassess my sales expectations going forward.

For "Other Products," revenue that exceeds $4 billion would support the view that Apple Watch and AirPods were strong sellers during the quarter. HomePod sales will also likely contribute to the year-over-year growth in revenue.

Revenue guidance that exceeds $50 billion would likely be viewed positively while revenue closer to $45B would be viewed negatively. It is likely that Apple's 3Q18 revenue guidance will reflect a year-over-year revenue increase. The increase is due to momentum in Services and Other Products.

Above Avalon subscribers have access to my full 5,000-word Apple 2Q18 earnings preview (four parts):

- Setting the Stage

- iPhone Estimates

- iPad, Apple Watch, Mac, Services Estimates

- Revenue, EPS, Capital Return, 3Q18 Guidance

Subscribers will also receive my exclusive earnings reaction emails containing all of my thoughts and observations on Apple's 2Q18 earnings report and conference call. To read my Apple earnings preview and receive my earnings reaction notes, sign up at the subscription page.