Above Avalon Podcast Episode 179: Winning the Buyback Debate

After years of criticism, doubt, and questions surrounding Apple’s share buyback program, we are at a point where we can say with confidence that the buyback debate has ended and Apple was declared the winner. In episode 179, Neil goes over how the buyback debate began and why so many people underestimated Apple’s ability to both buy back shares and invest in its future at the same time.

To listen to episode 179, go here.

The complete Above Avalon podcast episode archive is available here.

Subscribe to receive future Above Avalon podcast episodes:

RSS Feed (for your favorite podcast player)

Above Avalon Podcast Episode 178: Welcome to 2021

Episode 178 is dedicated to discussing Apple’s 2020 and where the company finds itself as we enter 2021. The episode goes over the first Above Avalon year in review that was published for 2020. Neil discusses his five favorite Above Avalon weekly articles from 2020 and the sub themes that were found in the 196 daily updates published in 2020.

To listen to episode 178, go here.

The complete Above Avalon podcast episode archive is available here.

Subscribe to receive future Above Avalon podcast episodes:

RSS Feed (for your favorite podcast player)

Apple Won the Share Buyback Debate

I receive many questions about Apple from Above Avalon readers, listeners, and members. In previous years, one topic has been far ahead of any other as a source of questions. Everyone wanted to know about Apple’s share buyback program.

Why is Apple buying back its shares?

Is Tim Cook trying to take Apple private?

Does buying back shares signal anything about Apple’s future product plans?

Why doesn’t Apple use cash to buy larger companies instead of buying back its shares?

Something interesting happened in 2020. I received far fewer questions about Apple’s share buyback program. To be precise, I didn’t receive an incoming question about buyback in nine months - from when the stock market put in a bottom in April 2020 to the start of 2021. What explains such a dramatic change? The Apple share buyback debate ended, and Apple was declared the winner.

How It Started

In the early 2010s, many on Wall Street viewed Apple as the iPhone company, and the iPhone was said to be “dead in the water.” A few activist hedge funds began circling around Apple shares due to their low valuation metrics relative to peers and the overall market. Apple was trading at a single digit forward price-to-earnings multiple – a valuation typically afforded to companies with little to no growth potential. On a free cash flow yield basis, Apple was priced like a junk bond.

In March 2012, after consultation with top shareholders, Apple announced it would begin paying a quarterly cash dividend and buying back shares. While Wall Street mostly applauded the move, Silicon Valley was convinced Apple had made a big mistake. Some thought Tim Cook was pressured into buying back Apple shares. Those who followed the “what would Steve Jobs do” doctrine were convinced that Cook had placed Apple on a path to ruin since Steve Jobs had famously viewed dividends and buyback as nothing more than distractions. At the time, none of Apple’s high-growth peers were buying back shares, which made Apple look even more like an outlier.

The primary concern held by those skeptical of Apple buying back shares was that by using cash to repurchase shares, Apple would have less cash to spend on capital expenditures (capex), research & development (R&D), and mergers & acquisitions (M&A). Said another way, some thought Apple was sacrificing its growth potential just to buy back shares.

Repurchase Pace

When looking back at Apple’s share buyback activity, one event stands out: passage of the Tax Cuts and Jobs Act of 2017. Prior to U.S. tax reform, Apple was constrained in terms of the amount of cash that could be spent on buyback. The company was penalized for bringing foreign cash back to the U.S. to fund share buyback. As shown in the exhibit below, Apple kept share buyback to a $30 billion to $45 billion per year pace despite having more than $150 billion of net cash on the balance sheet. Following U.S. tax reform, Apple was able to repatriate its foreign cash at more attractive tax rates. Apple’s share buyback pace shot higher and has been trending at $70 billion per year.

Exhibit 1: Apple Share Buyback Pace (Annual - FY)

Judging Apple’s Buyback Program

Since beginning to repurchase shares in 2013, Apple has spent $380 billion to buy back 10.6 billion shares at an average price of $35.80 per share. It’s tempting to think that Apple’s share buyback has been a success because Apple shares are trading 265% higher than the average price management paid to repurchase shares. However, one cannot judge buyback’s effectiveness or success by merely looking at the current stock price. Apple retires repurchased shares so there aren’t unrealized gains on the balance sheet from previously repurchased shares.

Share repurchases aren’t meant to boost stock prices even though some management teams may strive for such an outcome. Instead, share buyback is a tool for removing excess cash from balance sheets. In the process, a wealth transfer event is possible as ownership is shifted from shareholders willing to sell shares back to the company to those shareholders not selling shares. This is one reason why share buybacks are not created equally. Some companies incorrectly think buyback is a way to solve a problematic business model or lack of future growth while other companies see share buyback as a tool for balance sheet optimization.

The Above Avalon Report, “Share Buyback 101: An Examination of Apple’s Share Repurchase Strategy” contains much more detail on the wealth transfer dynamic found with share buyback. The report is available exclusively to Above Avalon members.

By repurchasing shares, a company doesn’t face brighter future prospects or even a higher stock price. The list of companies with stock prices that declined precipitously once share buyback concluded is long. Accordingly, a share buyback program’s effectiveness cannot and should not be judged by a company’s stock price.

End of Debate

Consensus agreed that Apple was holding on to too much cash on the balance sheet. However, there were differing opinions as to what Apple should do to remove the excess cash. Some thought that Apple should go on an M&A shopping spree. Twitter? Apple should buy it. Tesla? Apple should buy it. Netflix? Apple should buy it. Others thought Apple should ramp R&D so that as a percent of revenue, its R&D spending would be in line with that of its peers.

Instead of pursuing questionable expenditures such as large-scale M&A, paying special dividends, or simply saying “yes” to every R&D project imaginable, Apple instead saw an opportunity to both manage its balance sheet to a net cash neutral position (the amount of cash equals the amount of debt) and simultaneously invest in its future.

Apple’s share buyback debate didn’t end because Apple shares traded above a certain level, Apple repurchased shares below intrinsic value, or the company’s cash levels declined below a certain threshold. Instead, the buyback debate ended because Apple was able to successfully demonstrate that it can pile cash into buyback at record levels while also investing in its future at the same time. With Apple’s share buyback pace remaining at record levels, the company has been able to ramp up R&D to record levels while continuing to fund capex and pursue intelligent M&A.

What Did People Get Wrong?

Why did so many people underestimate Apple’s ability to both buy back shares and invest in its future at the same time?

People overestimated the amount of cash Apple actually needed to run the business and invest in the future.

People underestimated Apple’s ability to generate free cash flow.

As a percent of revenue, Apple’s R&D has historically been lower than that of its peers. Instead of this reflecting Apple underinvesting in R&D, the lower percentage reflects Apple’s unique culture and approach to product development. A better approach to take when judging Apple’s R&D spending is to compare current expenditures to historical totals. Apple spent more on R&D in FY2020 than the total it spent on R&D cumulatively from FY2010 to FY2014.

Apple’s capex needs are less than those of its peers. Apple has a capex-light business model because the company doesn’t offer free services to billions of people with a monetization strategy revolving around ads. This results in less property, plant, and equipment requirements.

Turning to M&A, Apple isn’t interested in buying products and users – a strategy that would likely be met with failure given the difficulty found with assimilating a target’s culture. Instead, Apple uses M&A to fill asset holes in the form of accessing technology and talent. This lends itself to Apple pursuing smaller deals involving companies with less in the way of thriving business models (and premium price tags).

Based on my estimates, Apple requires $10 billion to $15 billion per year to maintain and invest in property, plant, and equipment, and pursue intelligent M&A. Meanwhile, Apple’s business model predisposes the company to superior free cash flow generation. In FY2020, Apple generated a whopping $71 billion of free cash flow. The lack of significant capex requirements means that a high percentage of its operating cash flow ends up being free cash flow. As shown in Exhibit 2, Apple’s free cash flow has been increasing over time.

Exhibit 2: Apple Free Cash Flow (Annual - FY)

Apple’s superior free cash flow generation, combined with its investment run rate, allows the company to return tens of billions of dollars of excess cash to shareholders each year. This isn’t cash that would have been better suited for more R&D, capex, or M&A. Instead, the cash spent on buyback ends up keeping Apple management more disciplined and focused on proper and intelligent spending.

Big Picture

Apple has become a leader in corporate finance strategy. Following Apple, Google, Facebook, and Amazon have each subsequently announced their own share buyback program. Not surprisingly, none of them faced the kind of pushback that Apple faced during the last decade with its own buyback. Instead, Apple peers were applauded.

Consensus was convinced that Apple was buying back shares at the expense of its future growth potential. In reality, Apple’s growth potential has improved as its well-funded product strategy has allowed the company to pull away with the competition. In just the past five years, Apple has grown the iPhone installed base from 570 million to a billion users, and Apple’s ecosystem growth momentum is building. Apple’s wearables business has grown to the size of a Fortune 130 firm. Apple’s Services business went from a $20 billion to a $54 billion annual revenue run rate. In FY2020, Apple’s non-iPhone revenue growth, one of the best measures of ecosystem expansion, was 16%. Once consumers enter the Apple ecosystem via the iPhone, they proceed to buy additional Apple products and services.

There are still some questions worth asking regarding Apple’s share buyback. For example, with Apple shares trading at premium valuation multiples to the market, what is management’s approach to the buyback pace? However, when it’s a question of whether or not Apple management can buy back shares while also investing in its future, the debate has ended and Apple was declared the winner.

Listen to the corresponding Above Avalon podcast episode for this article here.

Receive my analysis and perspective on Apple throughout the week via exclusive daily updates (2-3 stories per day, 10-12 stories per week). Available to Above Avalon members. To sign up and for more information on membership, visit the membership page.

For additional discussion on this topic, check out the Above Avalon daily update from January 14th.

Above Avalon Year in Review (2020)

Heading into 2020, the big question facing Apple was found with growth. Apple had reached a billion users. Would Apple be able to reach two billion users in the 2020s by continuing to do what it had been doing or would more in the way of strategy shifts be needed?

As it did with every company, the pandemic turned 2020 into a steady stream of unexpected challenges for Apple. The company needed to figure out a way to continue product development on a global scale with little to no employee travel. Apple retail needed to be completely rethought as social distancing initiatives ruled out the usual crowded Apple stores. Apple events (both WWDC and product unveilings) needed to go virtual.

According to my estimate, Apple saw approximately $20 billion of delayed demand in FY2020 as a result of the pandemic. Approximately 15 million iPhone upgrades were delayed while wearables sales faced pressure due to retail stores being closed. Partially offsetting those headwinds, iPad and Mac results have been stellar as consumers upgrade older machines and look for larger displays to support working at home and distance learning.

Articles

In 2020, I published 15 Above Avalon articles. In looking through the articles, which are accessible to all, there was one overarching theme: Apple’s improving competitiveness in comparison to that of its peers and the steps the company is taking to position itself for continued ecosystem growth in the 2020s.

Here are some of my favorite articles published in 2020 (in no particular order):

Apple Is Pulling Away from the Competition. Relying on an obsession with the user experience, Apple is removing oxygen from every market that it plays in. At the same time, the tech landscape is riddled with increasingly bad bets, indifference, and a lack of vision. Apple is pulling away from the competition to a degree that we haven’t ever seen before.

The Secret to Apple's Ecosystem. Apple’s ecosystem remains misunderstood. There is still much unknown as to what makes the ecosystem tick. From what does Apple’s ecosystem derive its power? Why do loyalty and satisfaction rates increase as customers move deeper into the ecosystem? Apple’s ecosystem ends up being about more than just a collection of devices or services. Apple has been quietly building something much larger, and it’s still flying under the radar.

A Billion iPhone Users. A billion people now have iPhones. According to my estimate, Apple surpassed the billion iPhone users milestone last month. Apple’s top priorities for the iPhone include finding ways to keep the device at the center of people’s lives while at the same time recognizing the paradigm shift ushered in by wearables.

Apple’s $460 Billion Stock Buyback. Share buybacks came under fire earlier this year. Some companies that were recent buyers of their shares found themselves in financial distress and seeking bailouts due to economic fallout from the pandemic. A very good argument can be made that Apple has become the poster child of responsible share repurchases. The company has relied on its stellar free cash flow to fund share repurchases over the years.

Apple Watch and a Paradigm Shift in Computing. Despite being only four years old, the Apple Watch has fundamentally changed the way we use technology. Many tech analysts and pundits continue to look at the Apple Watch as nothing more than an iPhone accessory - an extension of the smartphone that will never have the means or capability of being revolutionary. Such a view is misplaced as it ignores how the Apple Watch has already ushered in a paradigm shift in computing.

The five most popular Above Avalon articles in 2020, as measured by page views, were identical to my favorites list.

Podcast Episodes

There were 16 episodes of the Above Avalon podcast recorded and published in 2020, totaling seven hours. The podcast episodes that correspond to my favorite articles are found below:

Charts

The following charts found in Above Avalon articles were among my favorite published in 2020.

Number of Users

While Apple new user growth rates have slowed, the company is still bringing tens of millions of users into the fold. Due to Apple’s views regarding innovation and its focus on the user experience, once someone enters the Apple ecosystem, odds are good that customer will remain in the ecosystem.

Apple Installed Base (Number of Users)

Apple Non-iPhone Revenue Growth

Apple finds itself in an ecosystem expansion phase. Hundreds of millions of people with only one Apple device, an iPhone, are embarking on a search for more Apple experiences. We see this with non-iPhone revenue growing by double digits in the back half of 2020 on a TTM basis, which is higher than growth rates seen in the mid-2010s.

Apple Non-iPhone Revenue Growth Projection

The Apple Innovation Feedback Loop

With Apple Silicon, Apple took lessons learned from personal devices such as Apple Watches, iPhones, and iPads to help push less personal devices, like the Mac, forward.

Daily Updates

In 2020, I published 196 Above Avalon Daily Updates that were available exclusively to Above Avalon members. With each update coming in at approximately 2,000 words, 196 updates are equivalent to seven books. This continues to be an industry-leading number when it comes to the amount of Apple business and strategy analysis published.

When looking over the topics discussed in this year’s daily updates, a few sub themes become apparent:

Apple and the Pandemic

When the pandemic began during the first half of the year, there was much unknown as to how a company like Apple would be impacted. It eventually became clear that Apple and its peers were positioned to do OK during the pandemic although new ways of thinking would be needed to navigate working from home and travel restrictions.

Big Tech Gaining Power in the Pandemic, Apple's Source of Power, Former Apple Industrial Designer Starts Speaker Company (May 28, 2020)

New iPhone Production Starting Soon, iPhone Production Estimates, Apple’s HW Solution for Pandemic Travel Restrictions (Sep 8, 2020)

Apple’s Place in a Stay-at-Home Economy, E-Commerce Acceleration, Some iPad and Mac Production Moving to Vietnam (Nov 30, 2020)

The Paid Video Streaming Battle

With Disney+ and Apple TV+ launching in late 2019 and HBO Max and Peacock launching this past May and July, respectively, 2020 turned out to be the legitimate start of the paid video streaming battle. As the true new kid on the block, Apple learned quite a bit about being more than just a distributor of other people’s content.

Apple Wins Ireland Tax Battle, Apple Hints at Apple TV+ Subscriber Total, Apple’s In-House Content Studio (Jul 15, 2020)

Thoughts on Early iPhone Sales, Disney Reorganizes, Disney Is Streaming’s New Poster Child (Oct 19, 2020)

A Video Content Distribution War, Roku and Amazon vs. Peacock and HBO Max, Microsoft Attacks the App Store (Jul 21, 2020)

Apple Sales Mix by Display Size, WarnerMedia’s Huge Movie Announcement, Apple and Movies (Dec 7, 2020)

Pushback Against the App Store

Apple is pulling away from the competition, and the App Store is considered the best (and last) chance for competitors to reshape the mobile industry to their liking. A series of legal and PR battles were waged against the App Store by a handful of smaller app developers and larger Apple competitors.

Tech CEOs Testify in Front of Congress, Congress’s Concern Regarding Apple, Apple’s Trouble Area (Jul 30, 2020)

Epic Games Breaks App Store Guidelines, Epic Games’ Epic Hypocrisy, The App Store’s Future (Aug 17, 2020)

The Coalition for App Fairness, A New Guerrilla Warfare Tactic, The Coalition’s Questionable Website (Sep 29, 2020)

The House Antitrust Report on Big Tech, Massive Holes in the Antitrust Report, Apple’s Response (Oct 8, 2020)

When looking at my daily updates published in 2020, selecting a handful of favorites out of 196 updates was not an easy task. The following updates stood out to me (in no particular order):

Apple’s Organizational Structure, Apple’s Leadership Structure, An Autonomous Apple. We first go over my thoughts on Apple’s functional organizational structure and the difference between a functional and multidivisional structure. The discussion then turns to Apple leadership and the ideas of “discretionary leadership” and “experts leading experts.” The update concludes with a revisiting of my Above Avalon article, “Jony Ive, Jeff Williams, and a Larger Apple” and a discussion of how Apple has been able to become a larger design company. (Oct 26, 2020)

Nike Earnings, The Similarity Between Nike and Apple, A Stronger Apple and Nike Partnership. We kick off this update with my thoughts on Nike’s earnings. After going over three structural tailwinds facing Nike, we discuss why I think Nike is pulling away from the competition. The discussion then turns to how Nike is the company most like Apple. The update concludes with a look at how Apple and Nike are both interested in health. We go over the competitive dynamic between the two companies and why it’s premature to conclude that Apple and Nike will become fierce competitors in the future. (Sept 24, 2020)

iPhone Momentum Building in Europe, Apple's Good Timing with iPhone SE, Selling Utility on the Wrist. We begin this update with my thoughts on the iPhone gaining momentum in Europe. The discussion includes new iPhone sales share data and what looks to be some kind of inflection point in the region. We also discuss the possible factors behind the inflection point. The update then turns to how Apple ended up launching the updated iPhone SE at just the right time. We then take a closer look at wearables competition on the wrist. In particular, we go over Fitbit’s latest earnings and compare fitness tracker and smartwatch demand. The discussion concludes with why Amazon Halo faces an uphill battle for wrist real estate. (Sep 3, 2020)

Valuing Big Tech on Free Cash Flow, AAPL vs. Free Cash Flow, AAPL vs. Low Interest Rates. This update begins with my thoughts on the idea that Wall Street has changed the way it is valuing Apple - one away from focusing on P/E ratios (price-to-earnings) and more towards free cash flow valuation. After going over the free cash flow yields for the tech giants, we look specifically at Apple’s declining free cash flow yield and what it tells us about how the market is approaching the company. The update concludes with a discussion of interest rates, inflation, and the U.S. Fed looking to embrace elevated inflation before seeing the need for higher rates. There are various AAPL-related implications associated with that development. (Aug 25, 2020)

Apple Acquires NextVR, Apple Glasses in 2022?, A Wearables Platform for the Face. We begin this update with my thoughts on Apple acquiring NextVR. The discussion includes the reasons why I think Apple acquired NextVR and how the company can play a role in Apple’s product strategy. The update then turns to new rumors about Apple Glasses launch dates. Simply put, the Apple AR / VR rumor mill is getting out of hand. We go over two factors that I think are driving the varied rumors regarding Apple Glasses. The discussion concludes with a different way of thinking about AR / VR and Apple. (May 18, 2020)

Warren Buffett’s Annual Letter, The Power of Apple Retained Earnings, Imploding Demand for Fitbit. We kick off this update by examining Warren Buffett’s annual letter to Berkshire Hathaway shareholders. Berkshire Hathaway is Apple’s largest individual shareholder. Accordingly, there is value in keeping on top of Berkshire and Warren Buffett (Berkshire’s CEO and Chairman of the Board). The discussion then turns to retained earnings and why Apple’s retained earnings are such a powerful tool. We conclude with a look at Fitbit’s awful 4Q19 earnings and why the company represents such a problem for Google. (Feb 24, 2020)

Here are the five most popular daily updates published in 2020 based on page views:

iPhone Sales Share Rises During Pandemic, It’s All About Smartphone Upgrading, A $5,000 Swiss Smartwatch (Jun 3, 2020)

Google Pixel Shakeup, Consumer Spending During the Pandemic, Surface Sales vs. iPad and Mac Sales (May 14, 2020)

Apple vs. Hey (Jun 17, 2020)

The App Store’s Impact on Apple Financials, Facebook Launches Paid Online Events, 4Q20 Microsoft Surface Results (Aug 18, 2020)

Just 11% of the daily updates published in 2020 are highlighted above. The full archive consisting of all 196 daily updates is available here. Membership is required to access the updates.

Daily Podcast (Launched in 2020)

In 2020, Above Avalon Daily Updates became available in audio for the first time via a private podcast called Above Avalon Daily. Reception to the daily podcast continues to exceed my expectations with very positive listener feedback. The podcast has allowed members to consume the daily updates in new and different ways while around the house, on a walk, or in the car. More information on the daily podcast, including a few sample episodes, is found here. Above Avalon Daily was launched in August, and 66 episodes were published in 2020, totaling nearly 17 hours of audio. Once a member signs up for the daily podcast, all prior episodes become available for listening in podcast players that support private podcasts.

Here’s to 2021

Without question, 2020 ended up being the busiest year for Apple since Above Avalon was launched in 2014. There was no shortage of newsworthy stories, and all indicators point to the fast pace continuing into 2021. A big thank you goes out to Above Avalon readers, listeners, and members for making 2020 another successful year for Above Avalon.

Above Avalon Podcast Episode 177: The Rise of the Small Display

While the pandemic is pushing people to embrace larger displays like iPads and Macs, the momentum found with smaller displays is still flying under the radar. In episode 177, Neil discusses how analysis of Apple device display size popularity can be used to gain insight into Apple’s ecosystem and quest to make technology more personal.

To listen to episode 177, go here.

The complete Above Avalon podcast episode archive is available here.

Subscribe to receive future Above Avalon podcast episodes:

The Rise of Smaller Displays

Apple is a design company selling tools capable of improving people’s lives. Approximately 80% of those tools include a display. Apple is shipping about 300 million displays per year, from iPhones and iPads to Macs and Apple Watches. With Apple running as fast it can towards AR glasses, the number of displays that the company ships will only increase over the next five to ten years. While the pandemic is pushing people to embrace larger displays like iPads and Macs, the momentum found with smaller displays is still flying under the radar.

Display Spectrum

Back in 2017, I published the following chart that tracks Apple device unit sales by display size. The exercise involved breaking out iPhone, iPad, and Mac unit sales by model - something that Apple has never done itself but which the company provided enough clues for me to do on my own and have confidence in the estimates.

Exhibit 1: Apple Device Sales Mix by Display Size (2016 data)

Since Apple offers a finite number of display choices, Exhibit 2 turns the sales data from Exhibit 1 into a broader statement about preferred display size.

Exhibit 2: Apple Device Sales Mix by Display Size (2016 data - Smoothed Line)

The motivation in pursuing such an exercise was to place context around the number of large displays Apple was selling in the form of MacBooks and iMacs. Fast forward three years, and it’s time to revisit the topic. With the significant amount of change occurring in Apple’s product line since 2016, there is value in going through a similar exercise regarding display size preference with 2020 unit sales in mind. While Apple’s financial disclosures haven’t gotten better over the past four years - if anything, the disclosures have gotten worse - I am still confident in my ability to derive unit sales estimates for all of Apple’s products.

Exhibit 3: Apple Device Sales Mix by Display Size (2020 data)

Exhibit 4: Apple Device Sales Mix by Display Size (2016 data - Smoothed Line)

(All of my granular estimates and modeling that went into Exhibits 3 and 4 is available to Above Avalon members in the daily update published on December 7th found here.)

As seen in Exhibits 3 and 4, there is bifurcation in Apple display size popularity. The most in-demand displays fall into two (broad) categories:

Displays large enough for consuming lots of video and other forms of content that can still be comfortably held in a hand or stored in a pocket.

Displays small enough to be worn on the body (Apple Watch) and products lacking a display altogether (AirPods).

It hasn’t been difficult to miss Apple’s gradual move to larger iPhone displays over the years. The 6.7-inch iPhone 12 Pro Max is getting close to the maximum size for an iPhone display, at least when thinking about the current form factor. Such a reality has undoubtedly played a role in some smartphone manufacturers betting heavily on foldable displays for smartphones. Such a bet boils down to believing consumers will want larger smartphone screens to the point of being OK with tradeoffs in terms of device thickness and weight. Move beyond the iPhone and display popularity plummets as the iPad and Mac sell at a fraction of the pace. There are small sales peaks found at 10.2 inches, the size of the lowest-cost iPad, and 13.3 inches, the size of the MacBook Air and entry-level MacBook Pro.

With hundreds of millions of people embracing 4.7-inch to 6.7-inch displays via iPhone, the claim that consumers are embracing larger screens over time contains some validity. Many are now wondering if similar moves to larger displays will take over the iPad and Mac lines. However, focusing too much on large displays will make it easy to miss what is happening at the other end of the spectrum. The rise of wearables has given an incredible amount of momentum to small displays and devices lacking a display altogether.

Implications

There are four key implications arising from this display bifurcation observation.

Apple’s ecosystem naturally supports the idea of multi-device ownership.

As devices are given more roles and workflows to handle, there is a natural tendency for screen sizes to increase without changing the overall form factor much.

Power and value are flowing to smaller displays that are capable of making technology more personal.

Devices relying on voice as an input make more sense when paired seamlessly with devices with displays.

It is worth going over each in greater detail.

1) Apple’s ecosystem is characterized by hundreds of millions of iPhone-only users buying additional Apple products and services. This is a result of industry-leading customer satisfaction rates and subsequently very strong brand loyalty. However, there are more fundamental themes underpinning this trend. By controlling hardware, software, and services, Apple is able to sell a range of products that seamlessly work together. These tools don’t serve as replacements for one another but rather as alternatives. This leads to consumers being able to use multiple Apple devices aimed at handling different workflows in their unique way. Such a dynamic supports the idea of multi-device ownership over time with those additional Apple devices likely containing smaller displays or no displays at all.

2) Apple has given the iPad, iPhone, and Apple Watch larger displays over time. For the iPad, the 12.9-inch / 11-inch iPad Pro and 10.9-inch iPad Air are larger than the initial 9.7-inch iPad and subsequent 7.9-inch iPad mini. The 3.5-inch display found with the first few iPhone models looks downright tiny next to iPhone 12 flagships. Even the Apple Watch was given a larger display after being sold for three years. These moves may seem to be unnoteworthy reactionary outcomes to competitors and market forces. However, the move to larger displays over time ends up being connected to the product category handling more workflows over time. iPhones have become “TVs” for hundreds of millions of people. Today’s iPad Pro flagships are geared toward content creation. Apple Watch faces are being given more complications in order to provide additional new-age app interactions to wearers.

3) The two product categories seeing the strongest unit sales momentum have either the smallest displays Apple has shipped (Apple Watch) or no displays at all (AirPods). As wearables usher in a paradigm shift in computing by altering the way we use technology, new form factors designed to be worn on or in the body for extended periods of time are playing a role in helping to make technology more personal. This leads to an observation that may not be so obvious: Smaller displays require new user inputs and interfaces that force new ways of handling existing workflows while supporting entirely new workflows. Said another way, smaller displays end up playing a vital role in lowering the barriers between technology and humans.

4) The reason stationary smart speakers were one of the biggest tech head fakes of the 2010s is that consensus incorrectly assumed the future was voice and just voice. The idea of voice as a user input being enhanced by the presence of a display was skipped over. Jump ahead a few years and the HomePod is arguably made better by having nearby displays either simply around us (iPhones) or on us (Apple Watch). Some of the magic found with AirPods involves the seamless integration with various displays, especially the Apple Watch display. Voice just isn’t an efficient medium for transferring a lot of data and context. Relying on displays for such context makes it possible for devices without displays to shine by being allowed to do what they do best - either provide superior sound (HomePod) or convenient sound (AirPods).

Bet on Smaller Displays

One takeaway from the pandemic has been that social distancing in the form of distance learning and working from home has fueled momentum for some of the largest displays in Apple’s product line. The iPad is setting multi-year highs for unit sales and revenue. The Mac registered an all-time revenue record last quarter. There are a few reasons behind this momentum that include families needing newer (and faster) machines and employers funding work-from-home upgrades.

Instead of looking at this development as the start of a new era for large displays, the momentum found with larger displays shifts focus away from the actual revolution taking place with smaller displays.

Apple is on track to sell approximately 150M devices in FY2021 that either lack a display or contain a display that is less than two inches (5 cm). We are still in the early innings of this revolution. Looking ahead at AR glasses, Apple will eventually sell devices containing two small displays for the first time. Relying on conservative adoption estimates, Apple will sell hundreds of millions of devices per year that contain either small displays or no displays at all. We are seeing the rise of smaller displays, and the secret to witnessing it is knowing where to look.

Listen to the corresponding Above Avalon podcast episode for this article here.

Receive my analysis and perspective on Apple throughout the week via exclusive daily updates (2-3 stories per day, 10-12 stories per week). Available to Above Avalon members. To sign up and for more information on membership, visit the membership page.

Above Avalon Podcast Episode 176: The Mac Earned a Diploma

The Mac is seeing momentum by being true to itself instead of trying to be something that it’s not. With a transition to Apple Silicon, the product category is now benefiting from lessons Apple learned from more popular devices aimed at the mass market. As the Above Avalon podcast enters its seventh season, episode 176 is dedicated to discussing the Mac’s Apple Silicon and what may come next for the Mac. Additional topics include the Apple Silicon transition being akin to a graduation for the Mac, the Apple Innovation Feedback Loop, and overlap between the iPad Pro and Mac portables.

To listen to episode 176, go here.

The complete Above Avalon podcast episode archive is available here.

Subscribe to receive future Above Avalon podcast episodes:

The Mac's Graduation

The iPad is seeing more than twice the number of new users as the Mac. Within two years, the number of people wearing an Apple Watch will equal the number of people owning a Mac. Approximately 90% of Apple users don’t use, and probably never will use, a Mac.

It’s tempting to look at the preceding statements and think that the Mac has lost its luster. However, 2020 was a record fiscal year for the Mac in terms of revenue and the number of new users was near a record high. How does one reconcile such different worlds? The Mac is seeing momentum by being true to itself instead of trying to be something that it’s not. With a transition to Apple Silicon, the product category is now benefiting from lessons Apple learned from more popular devices aimed at the mass market.

Apple Silicon Transition

This past June at WWDC, Apple unveiled the Mac’s multi-year transition to Apple Silicon. Last week, Apple’s “One More Thing” product event focused on the first wave of Mac hardware to take advantage of Apple Silicon. Three models saw updates:

13-inch MacBook Air

13-inch MacBook Pro

Mac mini

One of the more interesting takeaways from WWDC and last week’s event ended up being subtle. While Apple technically announced a Mac transition, the Mac ended up taking a back-row seat to the sheer power and capability found with Apple Silicon and Apple’s decade-long bet on designing its own chips.

A Graduation

The MacBook Air, Apple’s best-selling Mac, was included in the first wave of hardware transitioning to Apple Silicon. The well-known model had one of the more memorable unveilings in Apple history when it was pulled out of a manila envelope by Steve Jobs onstage at Macworld 2008.

The MacBook Air’s design was industry leading. Jony Ive and Apple’s industrial design group had utilized a new unibody architecture that was eventually brought to the entire Mac portable line. Twelve years later, the MacBook Air still feels refreshing.

While the MacBook Air’s thinness was the top feature in 2008, a MacBook Air powered by Apple Silicon is all about performance, longer battery life, and quietness. (The 12-inch MacBook that Apple unveiled in 2015 and discontinued four years later was ahead of its time.)

It is telling that Apple didn’t see the need to change the MacBook Air’s design despite the fact that it is being powered by Apple Silicon. This is evidence of the Apple Silicon transition being akin to the Mac graduating and entering a new phase in life.

A graduation is an acknowledgment of someone acquiring a certain amount of knowledge and experience. Such knowledge can then be used to solve future problems. A similar dynamic is found with Macs powered by Apple Silicon. The Mac now has a new toolset that it can rely on to tackle future problems.

Grand Unified Theory

Prior to this year’s WWDC, reaction in some tech circles was cool towards the idea of Apple transitioning the Mac to its own Silicon. Many were skeptical that Apple would want to face any risks and trouble that could be found with such a transition. Others figured the Mac wasn’t important enough to receive that kind of attention from Apple.

In reality, the Apple Silicon transition was always a question of when, not if. The transition would not only give Apple the kind of control over the Mac that it yearned for, but more importantly, Apple Silicon would open new doors to push the Mac forward in ways that simply weren’t possible with Intel.

With Apple Silicon, Apple took lessons learned from personal devices such as Apple Watches, iPhones, and iPads to help push less personal devices, like the Mac, forward. This is a core tenet of The Grand Unified Theory of Apple Products. We saw early iterations of this with Mac features such as the Touch Bar, Touch ID, and T1 / T2 chips. These additions were the clues that an eventual transition to Apple Silicon would take place.

What’s Next?

The Mac, having graduated thanks to Apple Silicon, is now in a much stronger position to navigate a world being overrun with iPhones, iPads, and an expanding line of wearable devices designed for different parts of the body (wrists, ears, and eventually eyes).

Based on my installed base estimates for various Apple product categories, as of the end of FY2020, it’s clear that the Mac hasn’t been for everyone:

There are 7x more people using iPhones than Macs. There are 2x more people using iPads than Macs. Some think that Apple Silicon will dramatically change these ratios by increasing the Mac’s addressable market. Caution is needed in running too far with such thinking.

The value found with Apple Silicon isn’t that it will turn the Mac into a fundamentally different product. We should not assume Macs will become touch-first devices. Apple already sells touch-first or touch-based computers; they are called iPhones and iPads.

For Apple, the goal isn’t to take fundamentally different product categories and form factors and converge them for no other reason than that they can. A far more challenging endeavor is to resist such calls from users, often the most loyal ones, and instead stay true to a form factor’s design.

When thinking about workflows, Apple’s iOS / iPadOS / macOS product lines are designed in such a way that some products do a better job of handling personal workflows than more demanding workflows. As shown in the following exhibit, macOS devices are designed to handle some of the most demanding workflows while iOS and iPadOS is geared toward handling more personal workflows. However, there is overlap between iPads running iPadOS and Mac portables running macOS when thinking about some workflows.

Since a MacBook Air and iPad Pro can handle some of the same workflows, some people think both devices will eventually merge into one another. The iPad Pro’s Magic Keyboard is positioned as a sign of this upcoming merge while touch-based Macs are said to be inevitable.

There are a few holes found in the logic of such thinking.

Even though Mac portables and iPads may handle many similar workflows, that doesn’t mean that both devices should lose their core identity. The iPad doesn’t move away from being a touch-based computer simply because a keyboard can be attached to it or an Apple Pencil can be used to take notes and sketch a drawing. A MacBook Pro doesn't embrace a touch-first interface just because Big Sur has similar elements to iOS and iPadOS.

Instead, we should expect Apple to take what makes the Mac special for 130 million people and accentuate those items, namely, a screen that tilts while always being attached to a dedicated keyboard. While both the screen and keyboard will likely see their fair share of changes in the future, including possibly sharing a foldable display, the dynamic found with using a keyboard permanently connected to a screen would remain.

While iPads would remain touch-first computers with a range of productivity accessories like dedicated keyboards, Macs powered by Apple Silicon could embrace multi-touch and foldable displays but in a dedicated area of the machine where one’s fingers are likely to always be found (think the area between the Touch Bar and the lower fifth of the screen). A good argument can be made that Apple should pursue flexible displays for Mac portables so that the entire area between the Touch Bar and vertical screen can be usable.

Such a product may seem underwhelming to some. The word “legacy” probably will come to mind for others. There is nothing inherently wrong with a product being classified as legacy as long as the product doesn’t jeopardize Apple’s ambition and efforts with new platforms and paradigm shifts. This risk was described in detail in the Above Avalon article titled “The Mac is Turning into Apple’s Achilles’ Heel.”

Apple management has spent the past few years trying to convince Mac users that the Mac’s future has never been brighter. Some pro users may end up disappointed with where Apple will, and won’t, take the Mac. However, it is a positive sign that Apple remains focused on pushing forward with new platforms aimed at lowering the barrier between technology and people while allowing the Mac to be true to itself.

Listen to the corresponding Above Avalon podcast episode for this article here.

Receive my analysis and perspective on Apple throughout the week via exclusive daily updates (2-3 stories per day, 10-12 stories per week). Available to Above Avalon members in both written and audio forms. To sign up and for more information on membership, visit the membership page.

Above Avalon Podcast Episode 175: iPhone at a Billion

According to Neil’s estimate, Apple surpassed the billion iPhone users milestone last month. With the iPhone upgrade cycle approaching a plateau of four to five years, Apple is well-positioned to report record iPhone unit sales. In episode 175, Neil discusses the current state of the iPhone business as it surpasses a billion users. Topic include: iPhone unit sales, iPhone sales mix broken out by iPhone upgrades and new users, the iPhone installed base, Apple’s top priorities for iPhone, peak iPhone, and more.

To listen to episode 175, go here.

The complete Above Avalon podcast episode archive is available here.

Subscribe to receive future Above Avalon podcast episodes:

A Billion iPhone Users

A billion people now have iPhones. According to my estimate, Apple surpassed the billion iPhone users milestone last month. Thirteen years after going on sale, the iPhone remains the perennial most popular and best-selling smartphone. Competitors continue to either shamelessly copy iPhone or, at a minimum, be heavily influenced by the iPhone. Looking ahead, Apple’s top priorities for the iPhone include finding ways to keep the device at the center of people’s lives while at the same time recognizing the paradigm shift ushered in by wearables.

iPhone Sales

Over the past two years, iPhone sales have experienced notable gyrations. In early 2019, Apple saw material weakness in iPhone sales due to deteriorating economic conditions in China related to U.S. trade tensions. Although Tim Cook faced some skepticism when making such a claim, the observation was later proven to be legitimate as a number of other companies went on to describe a similar slowdown in demand.

As shown in Exhibit 1, iPhone unit sales on a trailing twelve months basis dropped by about 12% in early 2019 from a 218 million annual pace to a 191 million pace. The iPhone business went on to experience a gradual improvement in sell-through (i.e. customer) demand during the second half of 2019 and the beginning of 2020 before the pandemic hit. iPhone unit sales are back above a 200 million annual pace and are currently 13% below the unit sales high experienced in 2015.

Exhibit 1: iPhone Unit Sales (TTM Basis)

At a glance, Exhibit 1 would suggest that the iPhone business has lost some of the shine it had in the mid-2010s. However, this would be a misreading of the situation. On its own, unit sales don’t tell us the full story about the iPhone business. This is the primary reason behind Apple’s decision in late 2018 to stop providing unit sales data on a quarterly basis. Wall Street was incorrectly using unit sales as a crutch for shoddy analysis.

Flat to down iPhone unit sales do not automatically mean iPhone business fundamentals have deteriorated. Instead, a longer upgrade cycle can be a leading factor behind declining unit sales. In addition, unit sales don’t say anything about customer loyalty and satisfaction rates, which are crucial when it comes to a customer’s decision to continue using a product.

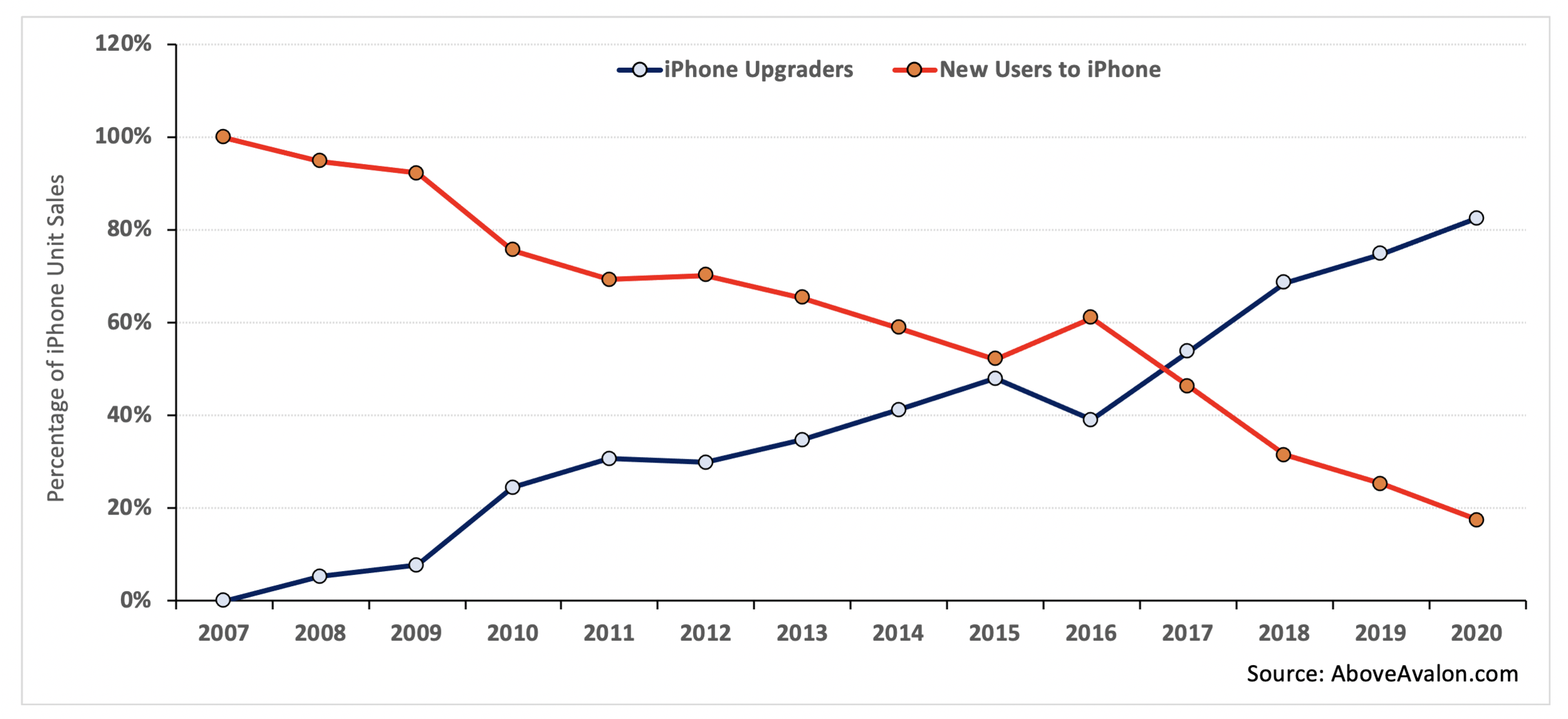

In order to reach more valuable insights regarding the iPhone business, Exhibit 2 takes unit sales data from Exhibit 1 and adds granularity. Instead of looking at sales just in terms of the number of units shipped from a factory, Exhibit 2 takes into account who bought iPhones: customers upgrading to a new iPhone or customers buying their first new iPhone. The data is derived from my iPhone installed base model that tracks when customers entered the installed base and then monitors upgrading patterns.

Exhibit 2: iPhone Unit Sales Mix (iPhone Upgraders vs. New Users to iPhone)

The iPhone business has turned into an upgrading business. While Apple is still bringing in 20M to 30M new iPhone users each year, the percentage of overall iPhone sales going to new users has steadily declined. For FY2020, iPhone sales to new users will likely have accounted for less than 20% of overall iPhone sales - an all-time low.

iPhone Installed Base

While quarterly iPhone unit sales contain an inherent amount of volatility, installed base totals do a better job of monitoring iPhone fundamentals over the long run. The iPhone installed base is defined as the total number of people using an iPhone (both new and used iPhones). A shrinking iPhone installed base would raise a number of warning signs for Apple as it would suggest people have been switching to Android. A growing iPhone installed base would suggest Apple continues to see new users embrace the iPhone for the first time.

Two variables are needed to estimate and track the iPhone installed base:

The number of people who purchase (and continue to use) a new iPhone from Apple or a third-party retailer.

The number of people who are using an iPhone obtained via the gray market. These iPhones have either been passed down through families and friends or resold to new users via a web of retailers and distributors.

By combining the two groups, one is able to derive estimates for the total number of iPhones in the wild. Although Apple does not disclose this installed base figure on a quarterly basis, the company did mention that the iPhone installed base surpassed 900M devices by the end of FY1Q19. As shown in Exhibit 3, which displays my estimates for the Apple installed base over the years, the iPhone installed base has grown each year since launch and recently surpassed a billion people.

(The methodology used to reach my iPhone installed base estimates is available here for Above Avalon members.)

Exhibit 3: iPhone Installed Base (total number of iPhone users in the wild)

In recent years, the pace of growth in the iPhone installed base has slowed. Much of this slower growth is due to high smartphone penetration and Apple having already successfully targeted the premium end of the smartphone market. With that said, Apple is still bringing in approximately 20M to 30M new iPhone users per year. These users are prime candidates for moving deeper into the Apple ecosystem by purchasing other Apple devices and services. Strong growth trends seen with iCloud storage, Apple’s content distribution services, Apple Watch, AirPods, and even iPad / Mac are made possible by hundreds of millions of people moving beyond just an iPhone to own additional Apple services and devices.

iPhone Priorities

Looking ahead, Apple has three primary priorities, or goals, for the iPhone:

Push camera technology boundaries.

Increase the value found with iPhone ownership.

Increase the number of roles handled by the iPhone.

Cameras. When thinking about the iPhone feature that will lead the way over the next five to ten years, more powerful cameras are high on the list. For the past few years, camera improvements and upgrades have been positioned as the top feature found with new flagship iPhones. A similar trend has been found with every major smartphone manufacturer. This has led to a type of camera arms race as each company tries to convince consumers that they have the best camera.

The primary reason Apple and its peers are betting so big on cameras is that they are convinced consumers will find value in smarter “eyes" - cameras that increasingly move into 3D rendering and AR realms. Advances in computational photography are also leveraged to make it easier for people to take really great photos.

While a bet on the camera will turn out to be a good one for Apple, the move doesn’t lack risk. As Apple pushes camera technology forward, many existing iPhone users are content with the iPhone camera they already own. This will manifest itself in no discernible bump in iPhone upgrading simply due to camera upgrades and advancements.

Another factor behind betting big on iPhone camera technology is that the smartphone form factor remains conducive to bringing powerful cameras to the mass market. While a “selfie” camera may make sense on the wrist with Apple Watch, it is difficult to see the wrist as a good place for cameras used to capture memories. There is similar hesitation found with the idea of putting such powerful cameras on the face in the form of AR glasses. Therefore, it makes sense that the device held in our hands and stored in our pockets will likely contain the most powerful camera in our lives.

iPhone Value. A major development regarding the iPhone that continues to fly under the radar is the improving value proposition found with owing and using an iPhone. By improving iPhone durability and longevity, Apple ends up strengthening the iPhone’s value proposition via higher resale values. If a new iPhone can be recirculated to additional users, the gray market will be strengthened and consumers will find more attractive payment terms and options at time of purchase.

An increasing number of iPhone users think about iPhone pricing in terms of monthly payments rather than lump sum. Attractive trade-in offers and payment plans with built-in upgrades only serve to improve the iPhone’s value proposition.

iPhone Roles. Tim Cook kicked off Apple’s “Hi, Speed” product event earlier this month by referring to the iPhone as the product we use the most, every day. He went on to say that the iPhone has never been more indispensable than it is now.

It is in Apple’s best interest to have the iPhone take over an increasing number of roles once given to laptops and desktops in addition to handling entirely new roles. By increasing our dependency on iPhone today, Apple ends up being in a better position to sell various wearable form factors tomorrow. Wearables are designed to not only handle entirely new tasks, but also take over tasks given to the iPhone.

Peak iPhone?

In FY2015, Apple sold 231 million iPhones. There continues to be a debate regarding whether or not Apple experienced “peak iPhone,” never exceeding that 231 million unit sales total in a 12-month stretch.

As a general rule, one needs to approach “peak” sales claims very carefully with Apple products. It may be tempting to look at unit sales data and conclude that a lower sales trend won’t reverse. However, weaker sales may not be the result of a change in market fundamentals such as a permanently reduced addressable market or less capable product. Instead, lower sales may simply reflect a slowdown in upgrading.

Odds are increasing that Apple has not experienced peak iPhone. As shown in Exhibit 4, my FY2021 iPhone unit sales estimate stands at 240M units, 4% higher than Apple’s previous iPhone sales record. My estimate does not assume a mega upgrade cycle kicked off by 5G iPhones. With the iPhone installed base having surpassed a billion users and continuing to expand by 20M to 30M people each year, Apple is in a good position to grow iPhone unit sales as the iPhone upgrade cycle plateaus between four and five years. This is where iPhone’s strong resale value enters the picture with consumers embracing various upgrading plans and options made possible by a well-functioning gray market.

Exhibit 4: iPhone Unit Sales (TTM Basis) - Includes Above Avalon FY2021 Estimates

New User Generation

The iPhone was the largest contributor to Apple growing its overall installed base from 125 million people in 2010 to more than a billion in 2020. Looking ahead, it’s fair to wonder if the iPhone will remain Apple’s primary new user funnel for the next billion users.

A strong case can be made that Apple will continue to rely on the iPhone for new user generation in the near term. While flagship iPhone pricing is aimed at the premium segment of the market, the gray market continues to play its role in expanding the iPhone’s reach to lower price segments.

Apple is also getting that much closer to launching its face wearables strategy. Requiring early versions of face wearables (AR / VR glasses) to work with an iPhone is logical when thinking about the limited amount of space for technology found with a pair of thin and light glasses.

Over time, we can’t ignore the new user growth potential found with Apple wearables. Apple Watch remains on its march to full independency from the iPhone. A truly independent Apple Watch would expand the product’s address market by threefold. AirPods are similarly well-positioned for appealing to Android users around the world. This brings us to India. The country will likely play a crucial role in Apple’s strategy of bringing hundreds of millions of new people into the ecosystem. As wearables make technology more personal, the product category’s addressable market will only expand.

While the iPhone may have been responsible for Apple getting to a billion users, wearables have a decent shot of getting Apple to two billion users.

Receive my analysis and perspective on Apple throughout the week via exclusive daily updates (2-3 stories per day, 10-12 stories per week). Available to Above Avalon members in both written and audio forms. To sign up and for more information on membership, visit the membership page.

Above Avalon Podcast Episode 174: Apple Watch Is a Runaway Train

While the tech press spent years infatuated with stationary smart speakers and the idea of voice-only interfaces, it was the Apple Watch and utility on the wrist that ushered in a new paradigm shift in computing. In episode 174, Neil discusses how Apple Watch momentum is building. The product category resembles a runaway train as no company is in a position to slow it down. Additional topics include the stationary smart speaker mirage, Neil’s Apple Watch installed base estimates, how Apple Watch derives its momentum, and Apple’s health platform.

To listen to episode 174, go here.

The complete Above Avalon podcast episode archive is available here.

Subscribe to receive the latest Above Avalon podcast episode:

Apple Watch Momentum Is Building

In a few months, the number of people wearing an Apple Watch will surpass 100 million. While the tech press spent years infatuated with stationary smart speakers and the idea of voice-only interfaces, it was the Apple Watch and utility on the wrist that ushered in a new paradigm shift in computing. We are now seeing Apple leverage the growing number of Apple Watch wearers to build a formidable health platform. The Apple Watch is a runaway train with no company in a position to slow it down.

Mirages and Head Fakes

We are coming off of a weird stretch for the tech industry. As smartphone sales growth slowed in the mid-2010s, companies, analysts, and pundits began to search for the next big thing. The search landed on stationary smart speakers and voice interfaces.

Companies who weren’t able to leverage the smartphone revolution with their own hardware placed massive bets on digital voice assistants that would supposedly usher in the end of the smartphone era. These digital voice assistants would be delivered to consumers via cheap stationary speakers placed in the home. Massive PR campaigns were launched that attempted to convince people about this post-smartphone future. Unfortunately for these companies, glowing press coverage cannot hide a product category’s fundamental design shortcomings.

At nearly every turn, Apple was said to be missing the voice train because of a dependency on iPhone revenue. Management was said to suffer from tunnel vision while the company’s approach to privacy was positioned as a long-term headwind that would lead to inferior results in AI relative to the competition. Simply put, Apple was viewed as losing control of where technology was headed following the mobile revolution.

There were glaring signs that narratives surrounding smart speakers and Apple lacking a coherent strategy for the future were off the mark. In November 2017, I wrote the following in an article titled, “A Stationary Smart Speaker Mirage”:

“On the surface, Amazon Echo sales point to a burgeoning product category. A 15M+ annual sales pace for a product category that is only three years old is quite the accomplishment. This has led to prognostications of stationary smart speakers representing a new paradigm in technology. However, relying too much on Echo sales will lead to incomplete or faulty conclusions. The image portrayed by Echo sales isn't what it seems. In fact, it is only a matter of time before it becomes clear the stationary home speaker is shaping up to be one of the largest head fakes in tech. We are already starting to see early signs of disappointment begin to appear…

I don’t think stationary smart speakers represent the future of computing. Instead, companies are using smart speakers to take advantage of an awkward phase of technology in which there doesn’t seem to be any clear direction as to where things are headed. Consumers are buying cheap smart speakers powered by digital voice assistants without having any strong convictions regarding how such voice assistants should or can be used. The major takeaway from customer surveys regarding smart speaker usage is that there isn’t any clear trend. If anything, smart speakers are being used for rudimentary tasks that can just as easily be done with digital voice assistants found on smartwatches or smartphones. This environment paints a very different picture of the current health of the smart speaker market. The narrative in the press is simply too rosy and optimistic.

Ultimately, smart speakers end up competing with a seemingly unlikely product category: wearables.”

Three years later, I wouldn’t change one thing found in the preceding three paragraphs. The smart speaker bubble popped less than 12 months after publishing that article. The product category no longer has a buzz factor, and despite the hopes of Amazon and Google, people are not using stationary speakers for much else besides listening to music and rudimentary tasks like setting kitchen timers.

The primary problem found with voice is that it’s not a great medium for transferring a lot of data, information, and context. As a result, companies like Amazon have needed to dial back their grandiose vision for voice-first and voice-only paradigms. Last week’s Amazon hardware event highlighted a growing bet on screens – a complete reversal from the second half of the 2010s.

Betting on the Wrist

As companies who missed the smartphone boat were placing bets on stationary speakers, Apple was placing a dramatically different bet on a small device with a screen. This device wouldn’t be stationary but instead push the definition of mobile by being worn on the wrist.

Jony Ive, who is credited with leading Apple’s push into wrist wearables, referred to the wrist as “the obvious and right place” for a different kind of computer.

When Apple unveiled the Apple Watch in 2014, wearable computing on the wrist was more of a promise than anything else. Apple created an entirely new industry – something that isn’t found much in the traditional Apple playbook.

After years of deep skepticism and cynicism, consensus reaction towards Apple Watch has changed and is now positive. Much of this is due to the fact that it’s impossible to miss Apple Watches appearing on wrists around the world. According to my estimates, approximately 35% of iPhone users in the U.S. now wear an Apple Watch. This is a shockingly high percentage for a five-year-old product category, and it says a lot about how Apple’s intuition about the wrist was right.

Apple Watch Installed Base

The number of people wearing an Apple Watch continues to steadily increase. According to my estimate, there were 81 million people wearing an Apple Watch as of the end of June. According to Apple, 75% of Apple Watch sales are going to first-time customers. This means that 23 million people will have bought their first Apple Watch in 2020. To put that number in context, there are about 25 million people wearing a Fitbit. The Apple Watch installed base is increasing by the size of Fitbit’s overall installed base every 12 months. Exhibit 1 highlights the change in the Apple Watch installed base over the years.

Exhibit 1: Apple Watch Installed Base (number of people wearing an Apple Watch)

(The calculations and methodology used to reach my Apple Watch installed base estimates is available here for Above Avalon members.)

Deriving Power

From where is Apple Watch deriving its momentum? The answer is found in The Grand Unified Theory of Apple Products.

One of the core tenets of my theory is that an Apple product category's design is tied to the role it is meant to play relative to other Apple products. The Apple Watch is designed to handle a growing number of tasks once given to the iPhone. Meanwhile, the iPhone is designed to handle a growing number of tasks given to the iPad. One can continue this exercise to cover all of Apple's major product categories.

Apple Watch is not an iPhone replacement because there are things done on an iPhone that can't be done on an Apple Watch. This ends up being a feature, not a bug. The Apple Watch’s design then allows the product to handle entirely new tasks that can’t be handled on an iPhone. This latter attribute goes a long way in explaining how Apple Watch has helped usher in a new paradigm shift in computing. Apple Watch wearers are able to interact with technology differently.

(More on The Grand Unified Theory of Apple Products is found in the Above Avalon Report, “Product Vision: How Apple Thinks About the World,” available here for Above Avalon members.)

A Health Platform

In January 2019, Tim Cook surprised many by saying Apple will be remembered more for its contributions to health than for any other reason. Here’s Cook:

“I believe, if you zoom out into the future, and you look back, and you ask the question, ‘What was Apple’s greatest contribution to mankind?’ it will be about health.”

Many assumed that Cook’s comment hinted at Apple unveiling a portfolio of medical-grade devices that would go through the FDA approval process. Such thinking was based on a fundamental misunderstanding of Apple’s ambition and approach to product development.

Apple’s health strategy is based on leveraging hardware, software, and services to rethink the way we approach health. This means Apple wasn’t going to just launch a depository for our health data – something that is needed but which ultimately falls short of being truly revolutionary. In addition, Apple wasn’t going to just offer health and fitness services that amount to counting steps or keeping track of miles run.

By the time Cook gave his bullish comment about health, Apple had already placed its big bet on health four years earlier by unveiling the Apple Watch. In what ended up being one of Apple’s best decisions, the company avoided going the route of medical-grade devices requiring government agency approval to reach consumers. Instead, Apple framed its health platform as a new-age computer that ultimately is an iPhone alternative.

Health monitoring is one of the key new tasks that the Apple Watch, not iPhone, handles. To be more precise, Apple Watch is handling the following four health-related items:

Proactive monitoring (i.e. heart rate and blood oxygen)

Well-being assistance (i.e. sleep monitoring including the runup to sleep)

Fitness and activity tracking (i.e. Activity and Workout apps)

Fitness and health activity (i.e. Apple Fitness+)

With Apple Fitness+, Apple didn’t just release a virtual fitness class service. Instead, Apple Fitness+ is an Apple Watch service. In some ways, Apple Fitness+ reminds me of Apple TV+. A future in which Fitness+ workouts are available on third-party gym equipment displays including on treadmills and stationary bikes is not a stretch. In addition, classes from other companies such as Nike could further elevate Apple Fitness+.

Competition

If the Apple Watch is a runaway train, there is no obvious candidate in a position to stop or even slow the train. While other companies are slowly waking up and seeing the momentum found with Apple Watch, there is still much indifference, mystery, and misunderstanding as to why people are buying wearables. Too many companies still think of wearables as glorified smartphone accessories. Such thinking makes it impossible for competitors to see how Apple Watch is ushering in a paradigm shift in computing by making technology more personal in a way that other devices have failed to accomplish or replicate.

One of the main takeaways from Apple’s product event earlier this month is how Apple is its own toughest competitor. The Apple Watch’s most legitimate competition is found with older Apple Watches and non-consumption (i.e. empty wrists). While this introduces its own set of risks and challenges, there is still no genuine Apple Watch competition from other companies after six years. This is an indication of the power found in controlling your own hardware, software, and services in order to get more out of technology without having technology take over people’s lives.

Listen to the corresponding Above Avalon podcast episode for this article here.

Receive my analysis and perspective on Apple throughout the week via exclusive daily updates (2-3 stories per day, 10-12 stories per week). Available to Above Avalon members in both written and audio forms. To sign up and for more information on membership, visit the membership page.

For additional discussion on this topic, check out the Above Avalon daily update from October 1st.

Above Avalon Podcast Episode 173: Let's Talk App Store

As Apple pulls away from the competition, the App Store is considered the best (and last) chance for competitors to reshape the mobile industry to their liking. In episode 173, Neil examines how competitors are waging a guerrilla war against Apple and the App Store. The discussion then turns to Neil unveiling a new podcast called Above Avalon Daily.

To listen to episode 173, go here.

The complete Above Avalon podcast episode archive is available here.

Attacking the App Store

Apple competitors have turned to guerrilla warfare tactics to wage a battle against Apple and the App Store. Based on what is being written and said about the App Store, one would think we have an entered a tech dystopia in which 27 million iOS developers and a billion Apple users are being taken advantage of by Tim Cook and his allegiance to Wall Street.

What had been valid criticism aimed at the App Store has descended into calls to burn everything down and replace it with anti-consumer and anti-developer alternatives. The writing is on the wall. Apple is pulling away from the competition, and the App Store is considered the best (and last) chance for competitors to reshape the mobile industry to their liking.

App Store

We have never seen anything like the App Store, a curated marketplace where a billion users can access 1.7 million apps. Apple established an easy, safe, private, and convenient way for consumers to personalize nearly 1.3 billion iPhones and iPads with third-party applications. Approximately 500 million people visit the App Store each week - a remarkable figure that speaks to how the App Store continues to connect with consumers on a global basis. In FY2019, App Store revenue was an estimated $53 billion. Apple’s share of that revenue came out to an estimated $14 billion. (Apple generates much less when it comes to App Store profit.)

Some have tried to say that there was a viable, safe, cost efficient, and overall compelling form of software distribution to the mass market prior to the existence of the App Store. There’s one problem with such a claim: The mass market didn’t consume software prior to the App Store. In 2008, the year the App Store launched, only 20% of people even had access to the internet.

There are a number of reasons why the iPhone installed base is eight times larger than the Mac installed base, and the App Store is high on the list.

Evolving Criticism

The App Store is not perfect. A small, but vocal, segment of the iOS developer community (now 27 million strong) has spent years raising concerns and issues regarding the App Store, and in particular, app review and the way Apple enforces App Store guidelines.

However, over the past 18 months, App Store criticism began to take on a dramatically different look and feel as multi-nationals entered the fray. In just the past few months, Facebook, Microsoft, Airbnb, and Epic Games have raised concerns about the App Store.

Spotify was one of the early App Store opponents. The company took what now looks like a delicate approach to raising specific issues with the App Store and what it deemed to be anticompetitive behavior on Apple’s part. While the company was grasping at straws with most of its claims, a few concerns had merit.

Microsoft decided to go behind Apple’s back to secretly get U.S. lawmakers to investigate the App Store on monopolistic grounds. Airbnb ran to the New York Times to air its grievance about wanting a special deal from Apple so it didn’t need to follow long-standing App Store guidelines.

However, it was Epic Games’ attack against Apple that marked a turning point in App Store criticism. Epic relied on a different kind of strategy:

Breaking App Store guidelines willingly and blatantly. We have never seen a company actually take pride in breaking App Store guidelines. Epic made sure everyone knew it was breaking App Store rules by offering a virtual currency as an in-app purchase without going through Apple payment.

Leveraging users and press to its advantage. Instead of making the battle be between two companies, Epic weaponized its user and fan base in an attempt to wage an uprising against Apple. In this pursuit, Epic also tried to use the press more than any other company that came before it in going after the App Store.

These corporations are ultimately after the same goal – to weaken Apple’s ironclad grip over the App Store. While many independent developers are simply focused on finding financial sustainability for their families, the multi-nationals are more interested in pulling iOS from under Apple’s control in order to gain power at the expense of Apple.

Why the App Store?

Apple is pulling away from the competition like never before. A revised product strategy (pull to push), and a broader consumer technology landscape that is swinging and missing on bet after bet, are the two primary factors behind Apple’s momentum. However, the App Store plays a vital role in setting Apple devices apart from the competition.

Accordingly, the App Store may seem like an unusual target for Apple competitors. The digital storefront is very popular with users (based on usage trends) and developers. (Most developers don’t pay Apple anything beyond a nominal developer fee to transact business through the App Store.)

No one is questioning the App Store’s success or popularity. Instead, competitors see a way to turn that success into a weakness. Due to extensive lobbying efforts, most of which were driven by Apple competitors, governments and regulatory bodies from around the world are investigating the claim that Apple is relying on monopolistic behavior to achieve App Store success.

Competitors see these regulatory investigations as a potential vulnerability in Apple’s armor. Breaking up or watering down the App Store would allow competitors to leverage the iOS ecosystem to their advantage. In essence, Apple would lose control over app distribution in its own ecosystem. Competitors would no longer be subject to revenue share arrangements with Apple. In addition, they would be able to establish their own digital storefronts to go direct to customers.

Guerrilla Warfare

Companies like Epic don't want there to be a genuine debate about the App Store. If the debate were to boil down to one’s experience using the App Store, Epic and other App Store critics would lose.

However, the goal is to change the narrative and position the App Store as being fundamentally broken with the only remedy being alternative app stores free from Apple oversight. This sentiment is summarized in the following tweet from Epic Games founder and CEO Tim Sweeney:

“At the most basic level, we’re fighting for the freedom of people who bought smartphones to install apps from sources of their choosing, the freedom for creators of apps to distribute them as they choose, and the freedom of both groups to do business directly.”

We are witnessing a guerrilla war that is being waged by Apple’s competitors. This campaign includes companies and CEOs trying to win the moral high ground by appealing to consumers’ and developers’ emotions. Other goals include trying to distract and tire Apple with relentless App Store attacks coming from all directions and using the press to do much of the heavy anti-App Store lifting.

Nearly every article written about Apple’s latest App Store controversy and battle inevitably includes paragraphs of boilerplate language regarding the App Store’s growing list of regulatory issues around the world. Meanwhile, no space is dedicated to the holes and hypocrisy found in competitors’ claims and allegations against the App Store. This is a classic example of a PR guerrilla warfare tactic utilized by competitors in an attempt to sway the discussion and public opinion.